Oil Market Forecast - May 2022

Summary

This month sees some further downgrades in oil demand estimates for the year and continued uncertainty on the impact of the Russian invasion of Ukraine on global supply. The market looks to be in deficit through the forecast period and the surplus of stored crude that was built up over the last couple of years has now been worked off. There are early signs of physical shortages of oil products in some parts of the world, while crude oil prices have retreated from last month’s highs. The US rig count continues its steady climb while the US Interior Department canceled a number of lease sales planned for this year.

A few key points:

- The EIA and OPEC cut their 2022 demand estimates again this month, while the IEA held theirs steady which leaves the range of estimates for the year between 99.4 MMbbl/day and 100.3 MMbbl/day.

- European Union efforts to impose an import ban on Russian oil appear to have stalled in the face of opposition from Hungary and Slovakia

- API members are split over a proposal to lobby US Congress to adopt a carbon tax.

- OPEC+ raises their production target for June by 432,000 bbl/day.

- The oil market is undersupplied through the forecast period, with a supply deficit of 1 – 2 MMbbl/day this year.

- Shortages of diesel, gasoline and jet fuel have been reported across sub-Saharan Africa.

- Spot and futures prices eased back from last month’s highs, but remain above $100/bbl.

- The US oil land rig count rose from 535 last month to hit 545 on May 13th.

- More than half of US publicly listed oil company executives identified capital discipline as the primary reason they were restraining production growth.

- The Interior Department cancelled two lease sales in the Gulf of Mexico and one in Alaska.

Oil Supply and Demand

The IEA held their 2022 oil demand estimate steady at 99.4 MMbbl/day (1). OPEC cut their 2022 demand forecast by 200,000 bbl/day, from 100.5 MMbbl/day last month to 100.3 MMbbl/day this month (2), citing a slowdown in global growth and the impact of a COVID-19 outbreak in China. The EIA cut their 2022 demand estimate the same amount, from 99.8 MMbbl/day to 99.6 MMbbl/day, again citing concerns about growth in China (3). The EIA also cut their 2023 demand estimate by the same margin, bringing that down to 101.5 MMbbl/day.

This month saw news that could impact oil demand over the short, medium, and long term. Dealing with the short term first, the European Union (EU) has been moving towards a ban on the import of Russian oil and oil products as part of their sixth sanctions package in response to the Russian invasion of Ukraine. At the time or writing, it was not clear whether this would move forward (4), as Hungary and Slovakia remain resistant to any import ban. As landlocked nations, Hungary and Slovakia rely on pipelines to deliver oil from Russia, making it much more difficult to source alternate supplies.

An EU ban would have a significant impact on both the oil markets and the Russian economy. The EU imports 3.1 MMbbl/day of crude and Natural Gas Liquids and 1.5 MMbbl/day of oil products from Russia. Some of those volumes will have been impacted by formal sanctions, and the reluctance of some trading companies to deal in Russian crude. Still, an import ban, even the kind of phased import ban that the EU is discussing, would result in some shut in production, at least for a period while Russia re-oriented its exports. Russia is also being forced to sell those re-oriented exports at a sharp discount - $30/bbl is the widely quoted figure – so even if Russian export levels eventually recovered, revenues would suffer.

Both the EIA and OPEC cited the COVID-19 outbreak in China as a basis to downgrade their demand estimates. Nomura reported this week that 41 cities, account for 30% of China’s GDP were in full or partial lockdown (5). Reuters reported that Chinese crude oil imports were down by 4.8% in the first four months of 2022, compared to the prior year (6), although imports did climb in April.

In the medium term, an already tight oil market, exacerbated by the Russian invasion, has driven oil prices above $100/bbl at exactly the same time as mainstream auto manufacturers begin to roll out their electric vehicle line ups. High oil prices should provide a tailwind to electric vehicle sales as consumers in the market for a new vehicle look for ways to insulate themselves from rising fuel costs. Rising electric vehicle sales will, in turn, provide a headwind to rising global oil demand. As Tesla recently reported (7), however, oil is not the only commodity that has seen recent inflation. Tesla highlighted the soaring cost of lithium as the reason they have had to raise their prices. While higher prices have had no impact on Tesla’s sales figures, other electric vehicle manufacturers may face more of a struggle to convince the public to go electric.

Looking at longer term trends, The Wall Street Journal (8) reported that the American Petroleum Institute (API) membership has split over an API proposal to implement a carbon tax. The draft proposal, yet to be approved by the API’s executive committee, would urge Congress to impose a carbon tax of $35/ton to $50/ton. The measure is supported by some European members such as Shell and Equinor but opposed by a number of US refiners and Independents.

The author’s own opinion is that a carbon tax is the most efficient way to limit carbon dioxide emissions – it places a price on the thing that causes the problem and lets the market, rather than politicians, resolve it. The author is also coming around to the view that a carbon tax is politically impossible in the US, as the electorate is simply too sensitive to gasoline prices. The opposition to the API’s initiative appears to stem from a combination of doubt that it would ever be passed, together with the recognition that it would alienate political allies. The Republican Party will attempt to paint the Biden administration’s policies as responsible for energy price inflation in this year’s mid-term elections. Having to explain away a policy proposal from the industry that would push them up even further would be a huge electoral liability. Neither will the proposal win the API any friends among the Democrats, whose climate change policies are more focused on incentivizing a transition to alternatives rather than taxing carbon.

On the supply side, OPEC+ stuck to their guns and raised their output target for June by 432,000 bbl/day, which takes total target OPEC+ production to 42,558 MMbbl/day. Going back to the 19th OPEC and Non-OPEC Ministerial Meeting of July 18th, 2021 (9), reference OPEC+ production levels for May 2022 were 45,485 MMbbl/day. Not only is the current OPEC+ target nearly 3 MMbbl/day short of their reference production level, as reported over the last few months OPEC+ is struggling to achieve even that, lower, target. The IEA did not publish April figures in their May Oil Market Report, but in March OPEC+ production was 1.63 MMbbl/day below target.

The Russian oil industry is struggling to adjust to formal and informal sanctions on exports of Russian oil. In late April Rosneft tried and failed to auction close to 38 MMbbl of oil (10). Rosneft was forced to run the sale itself as the trading companies it normally relies upon were unwilling to handle the sale. The exact impact on production will soon become more difficult to gauge as Russia’s Energy Ministry has announced that it will limit access to statistics on Russian oil production and exports (11). The intent may be to make Russian oil harder to track, making it easier to evade sanctions. The Wall Street Journal reported a spike in Russian crude oil exports to ‘destination unknown’ in April. This designation is often used by sanctioned countries such as Iran and Venezuela to disguise the origin of their oil.

In the medium term, there does appear to be, if not a renewed embrace of fossil fuels, then perhaps a more positive tone from investors. Last week Blackrock announced that it wouldn’t be able to support as many pro-climate environmental or social proposals as it had in the past, arguing that these were becoming increasingly prescriptive and constraining (12). This change of posture may signal a growing willingness to invest in the oil & gas industry.

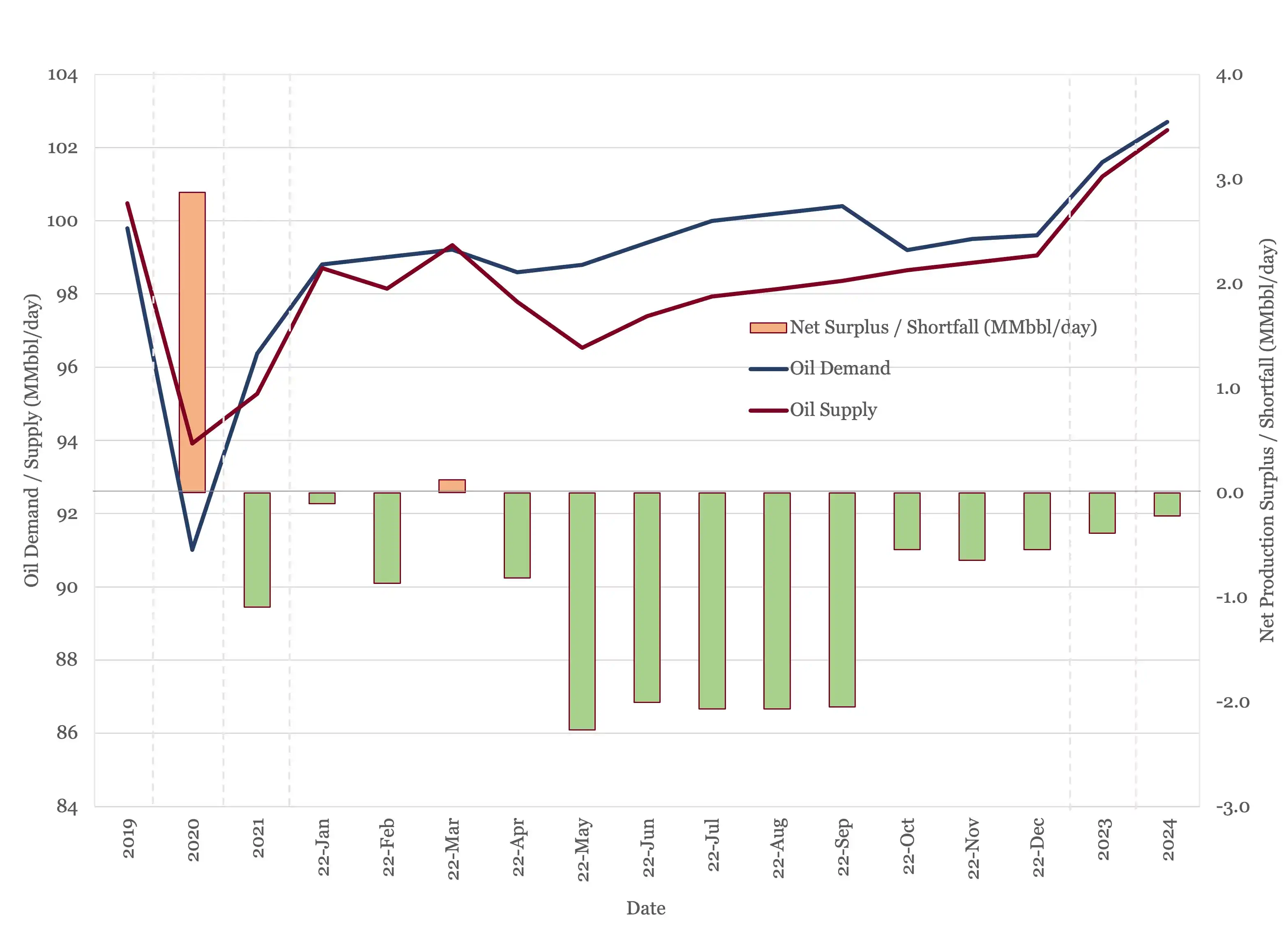

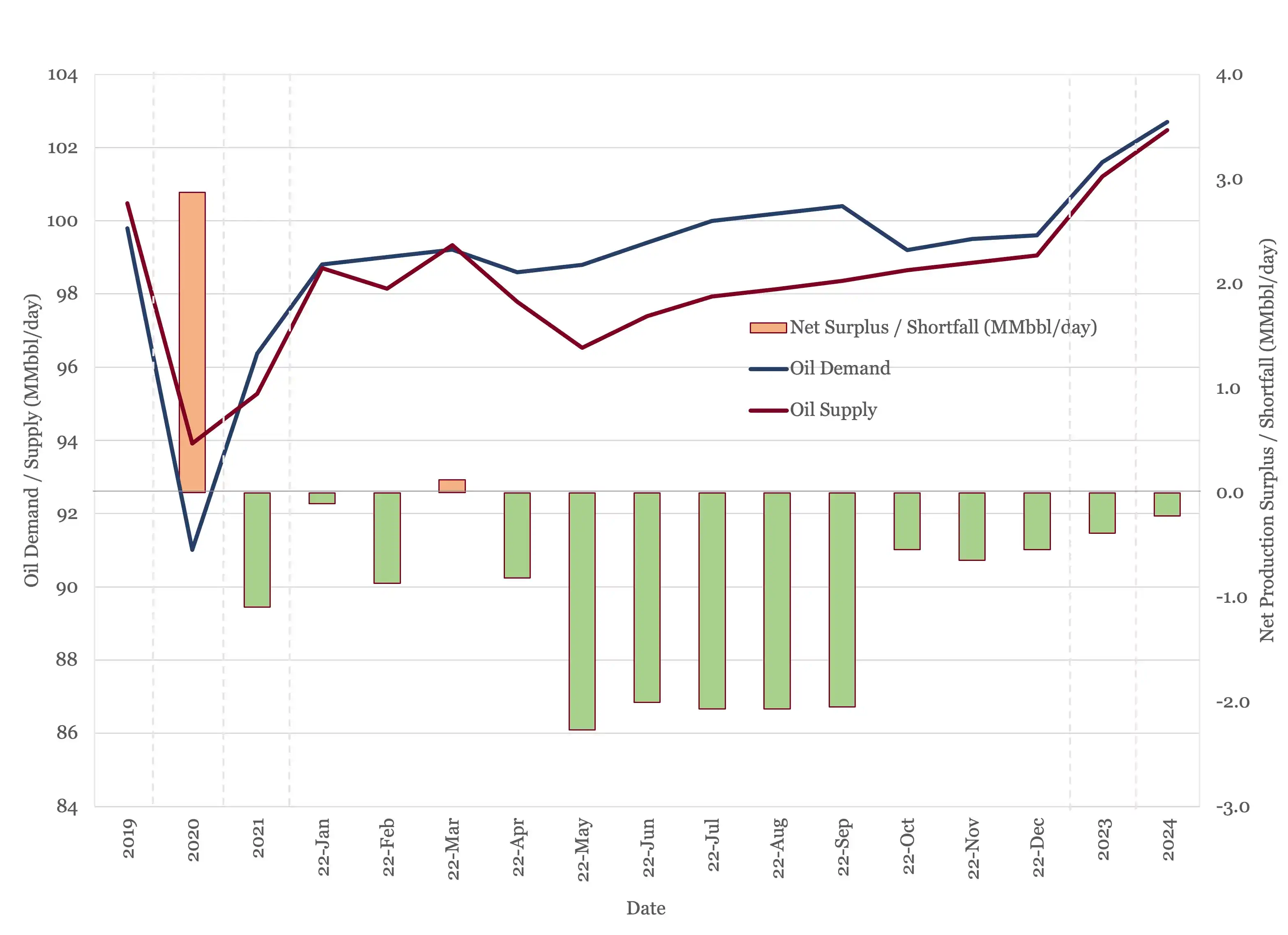

Overall, the impact of formal and informal sanctions appears to be less severe that had been predicted last month. In their latest Oil Market Report, the IEA think that production was down by 1 MMbbl/day in April, rather than the 1.5 MMbbl/day that they had estimated the month before. The drop in May is likely to be sharper, as the sanctions that were announced in March did not come into full effect until the 22nd of April. The net effect is that the oil market remains in a deficit through the rest of the forecast period, as shown in Figure 1.

Figure 1 - Supply and Demand Surplus Forecast

Oil Storage

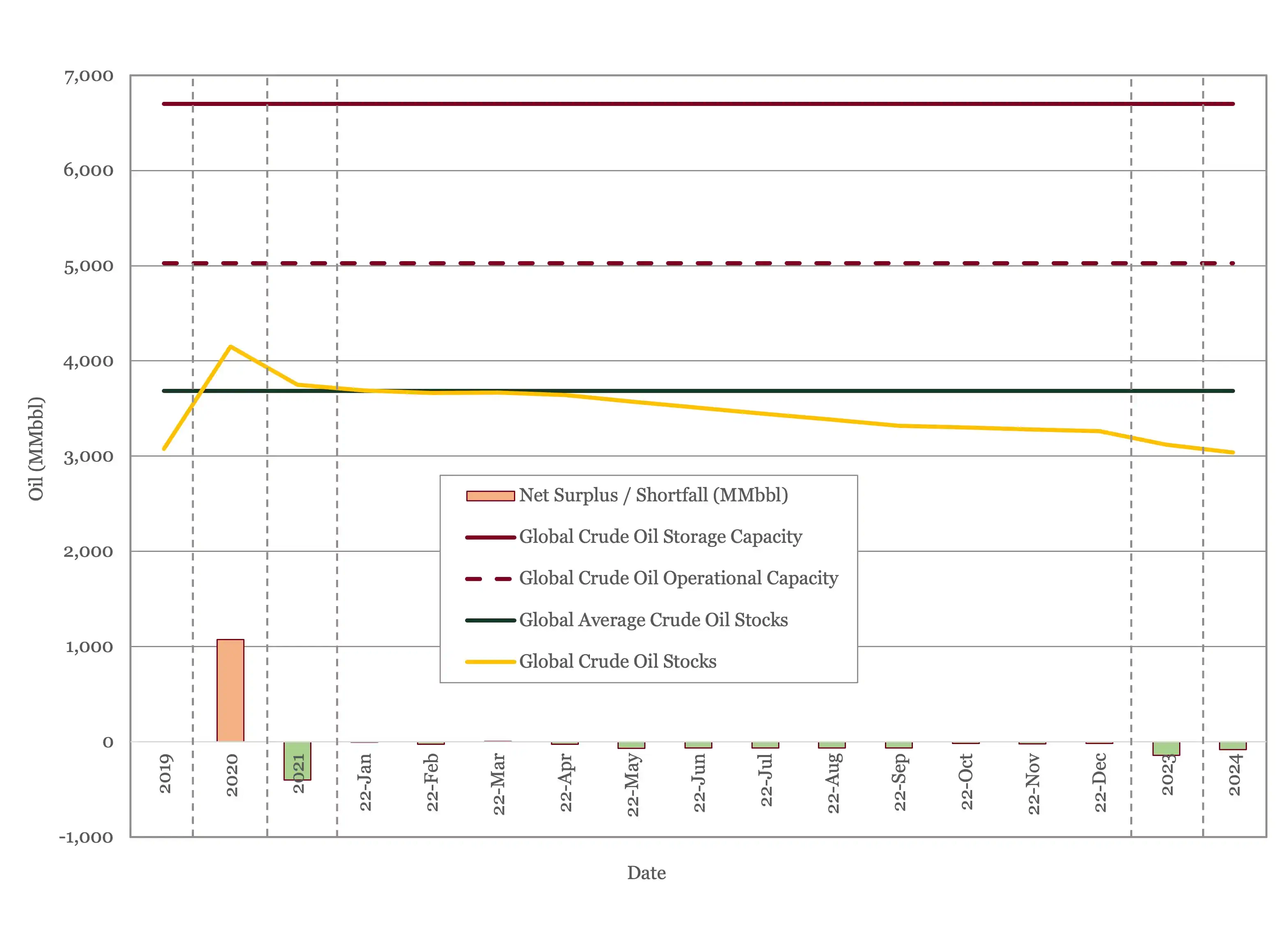

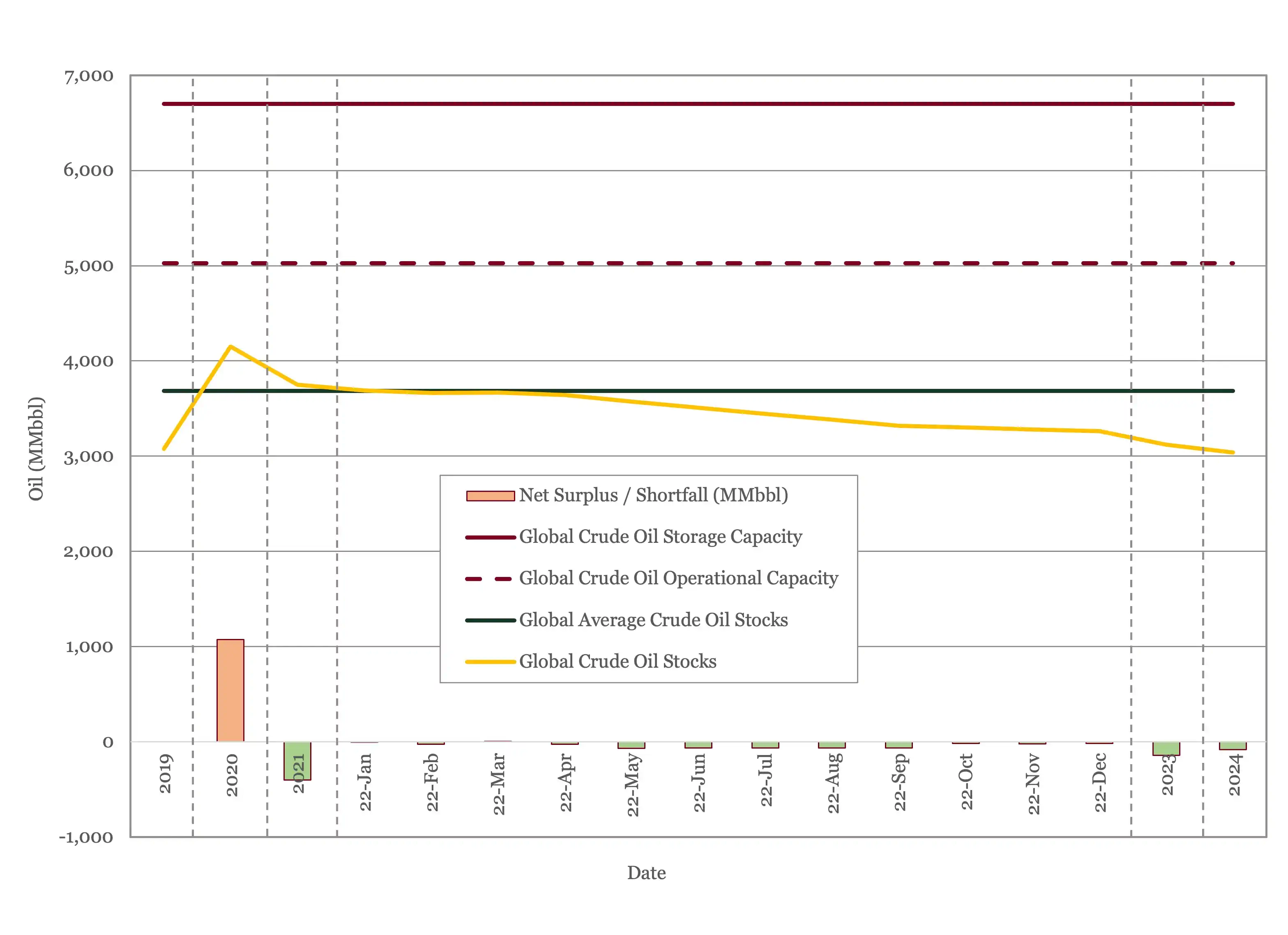

Global oil inventory drawdowns for 2022 are down from last month’s estimates, on higher forecast US production, at 488 MMbbl. This is still below the overall build of 1,072 MMbbl in 2020 but combined with stock draws of 321 MMbbl last year we are below the 5-year average now and stocks will fall below 2019 levels by year end. The EIA estimates that OECD inventories are 315 MMbbl below their 5-year average.

Figure 2 - Global Storage Chart

While OECD stocks are running low, across sub–Saharan Africa, there are real fuel shortages. Last week the Economist reported physical shortages of jet fuel, gasoline and diesel in Senegal, South Africa, Cameroon, Kenya, and Nigeria (13). The physical shortages have reached Africa first due to a combination of factors. The current backwardation in the Brent futures market is driving traders to sell crude immediately into Asian markets, rather than use floating storage offshore west Africa, where local traders can pick up small volumes as those tankers pass by. Hedging costs for local traders are increasing in line with the oil price, forcing those unable to expand their balance sheets to reduce imports. Africa has little domestic refining capacity, which is why people are forced to queue for fuel in Nigeria, a major crude oil exporter, and most countries in sub-Saharan Africa do not maintain supplies in reserve, as is common in the OECD. Maintaining a strategic reserve does not eliminate the risk of shortages, it just delays them. The longer the current production deficit persists, the more nations will start to see this type of supply shortage.

Oil Prices

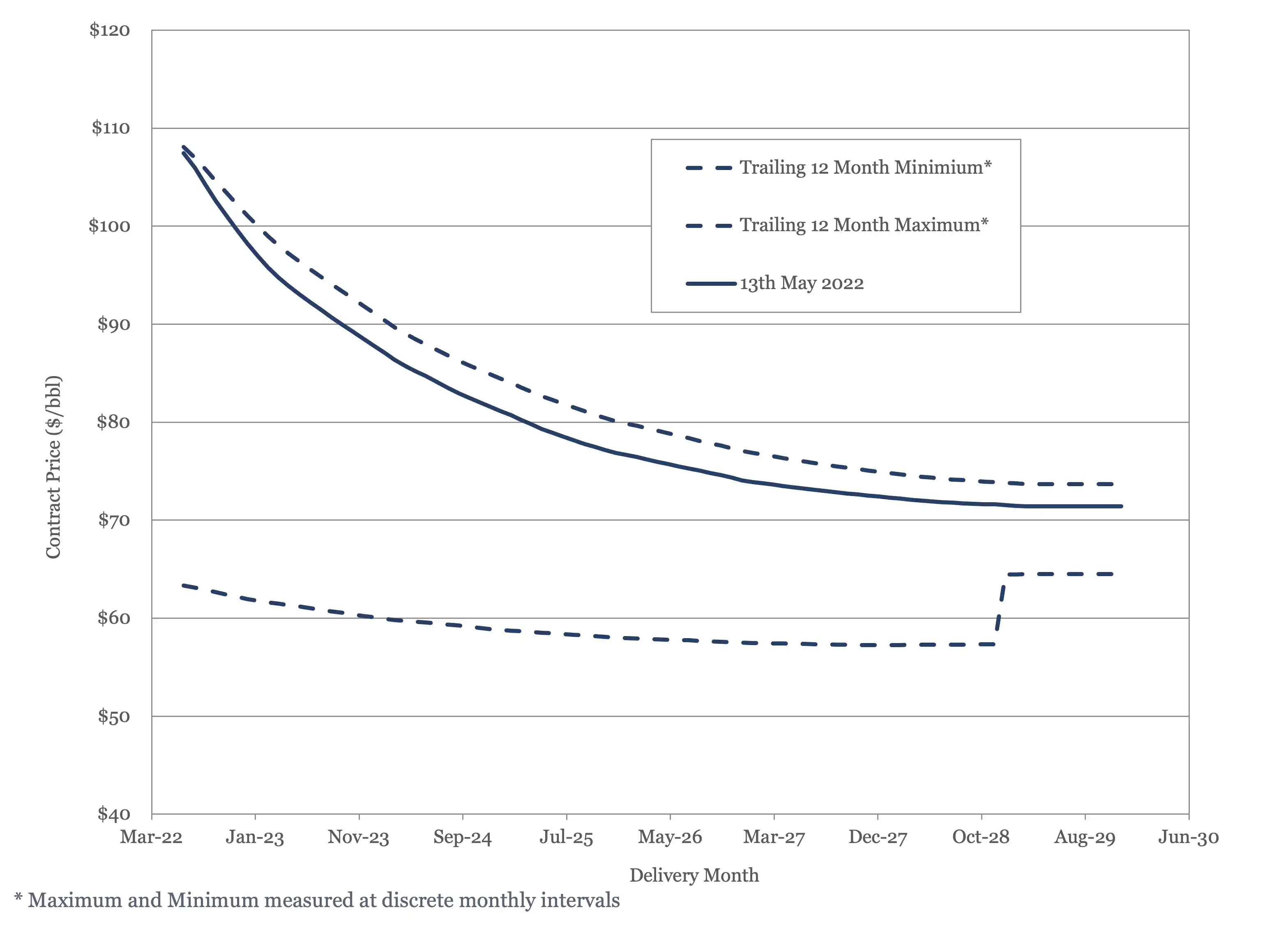

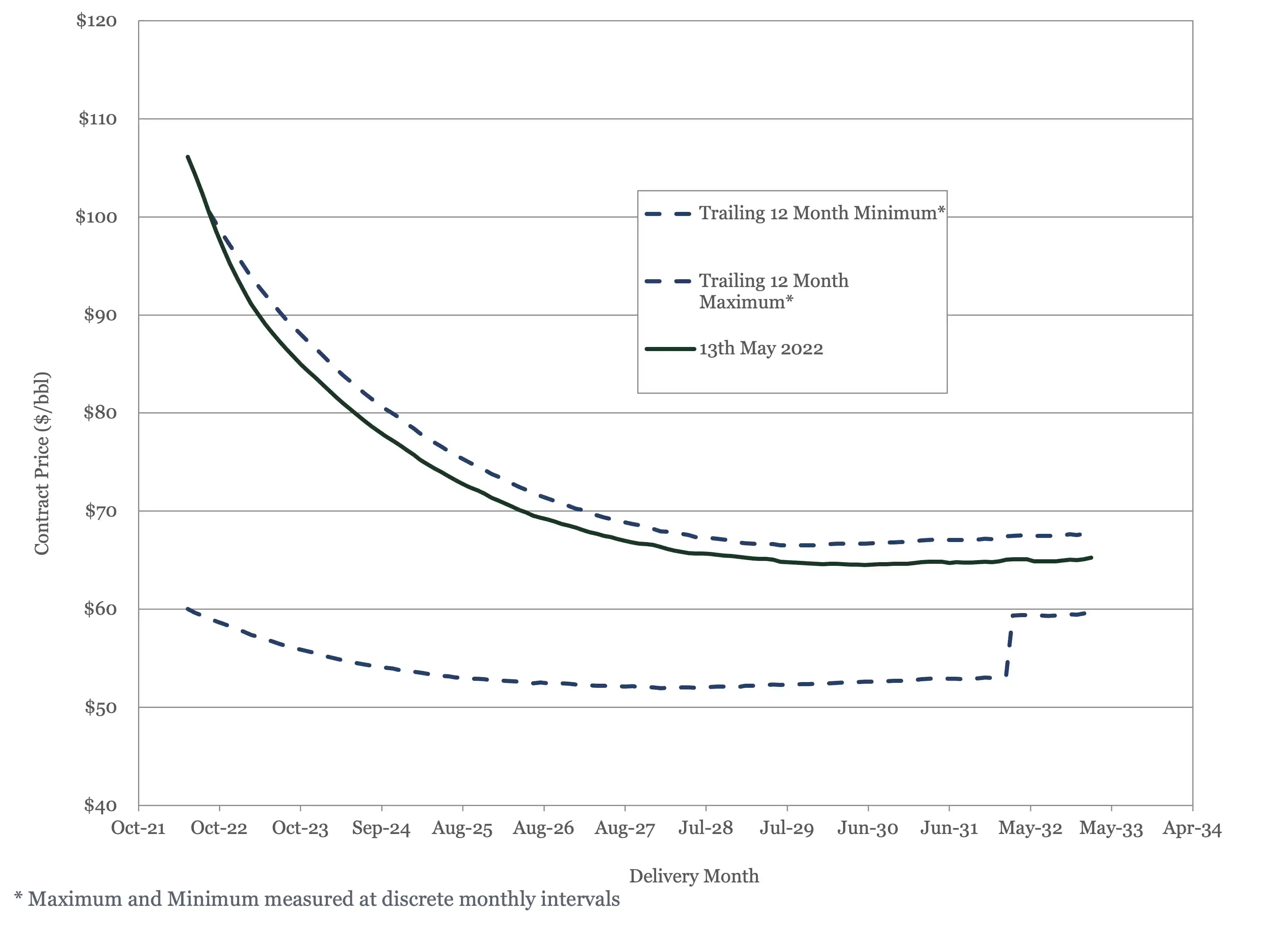

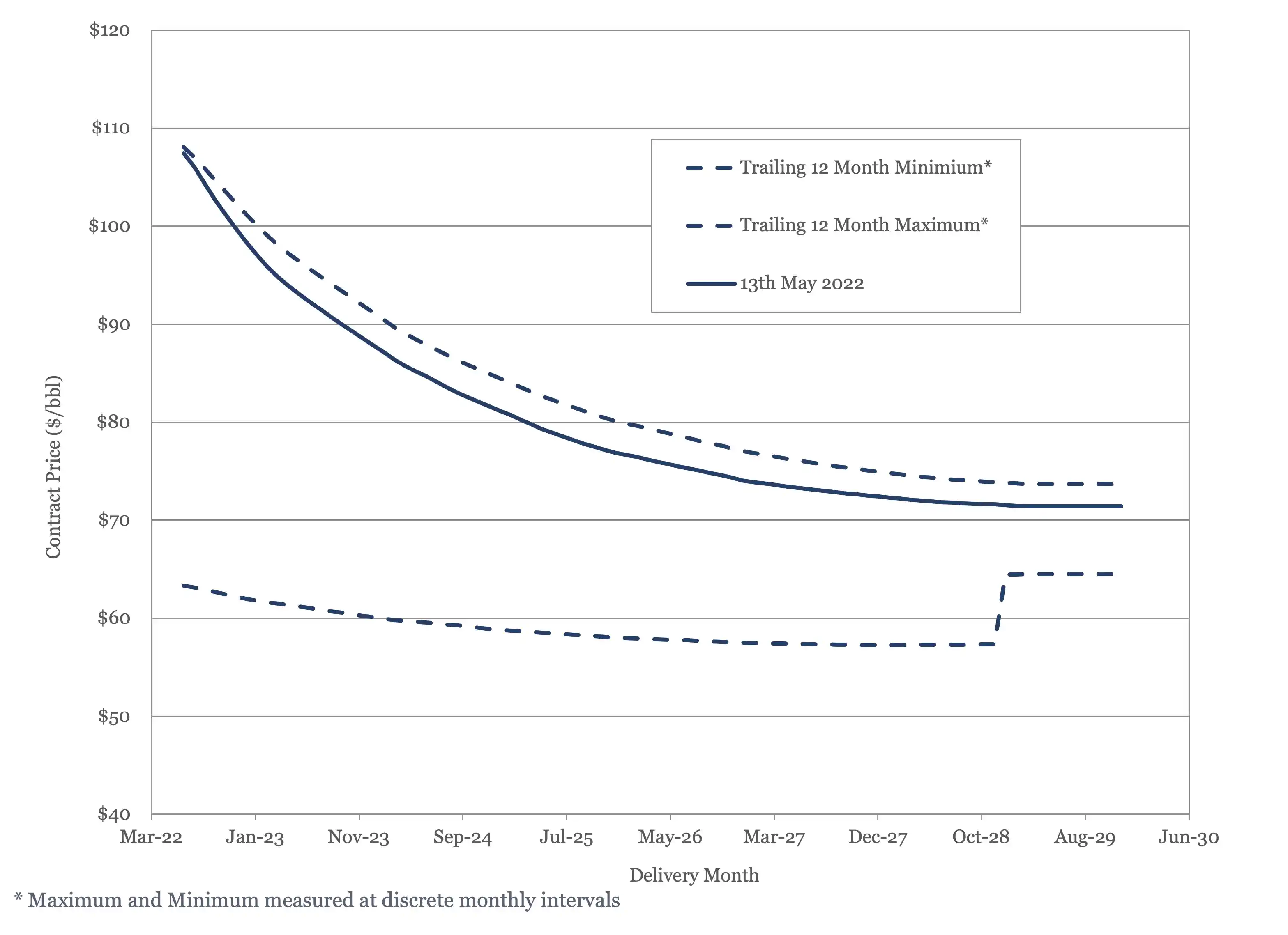

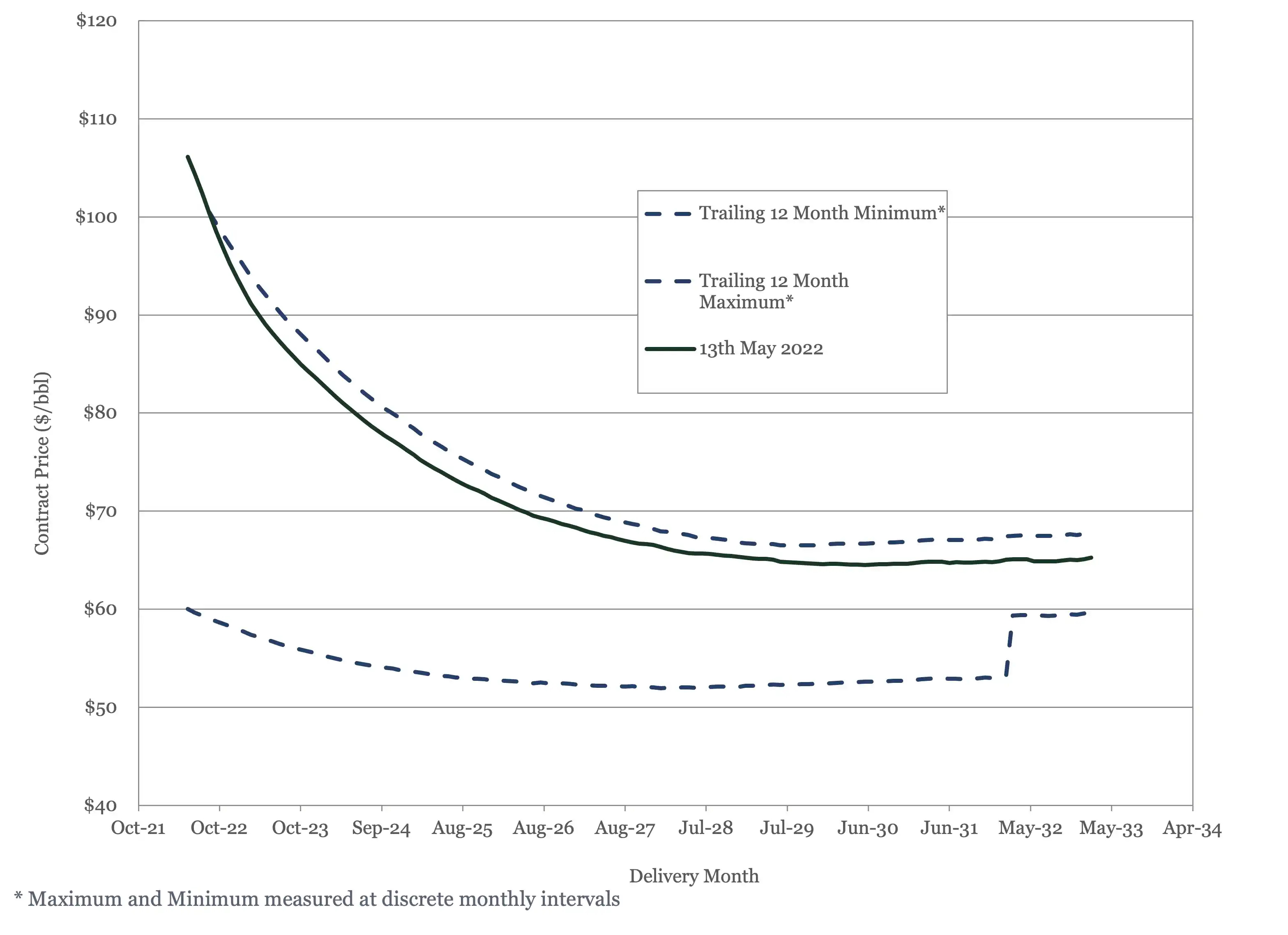

Both Brent and WTI spot and futures prices were down this month, but $100/bbl appears to be a floor. The EIA raised their estimate for 2023 prices by $5/bbl to $97/bbl. The Center for Strategic and International Studies warned that EU sanctions on Russian oil would be likely to push prices sharply higher again (14).

Figure 3 - Brent Crude Oil Futures

Figure 4 - WTI Crude Oil Futures

US Activity

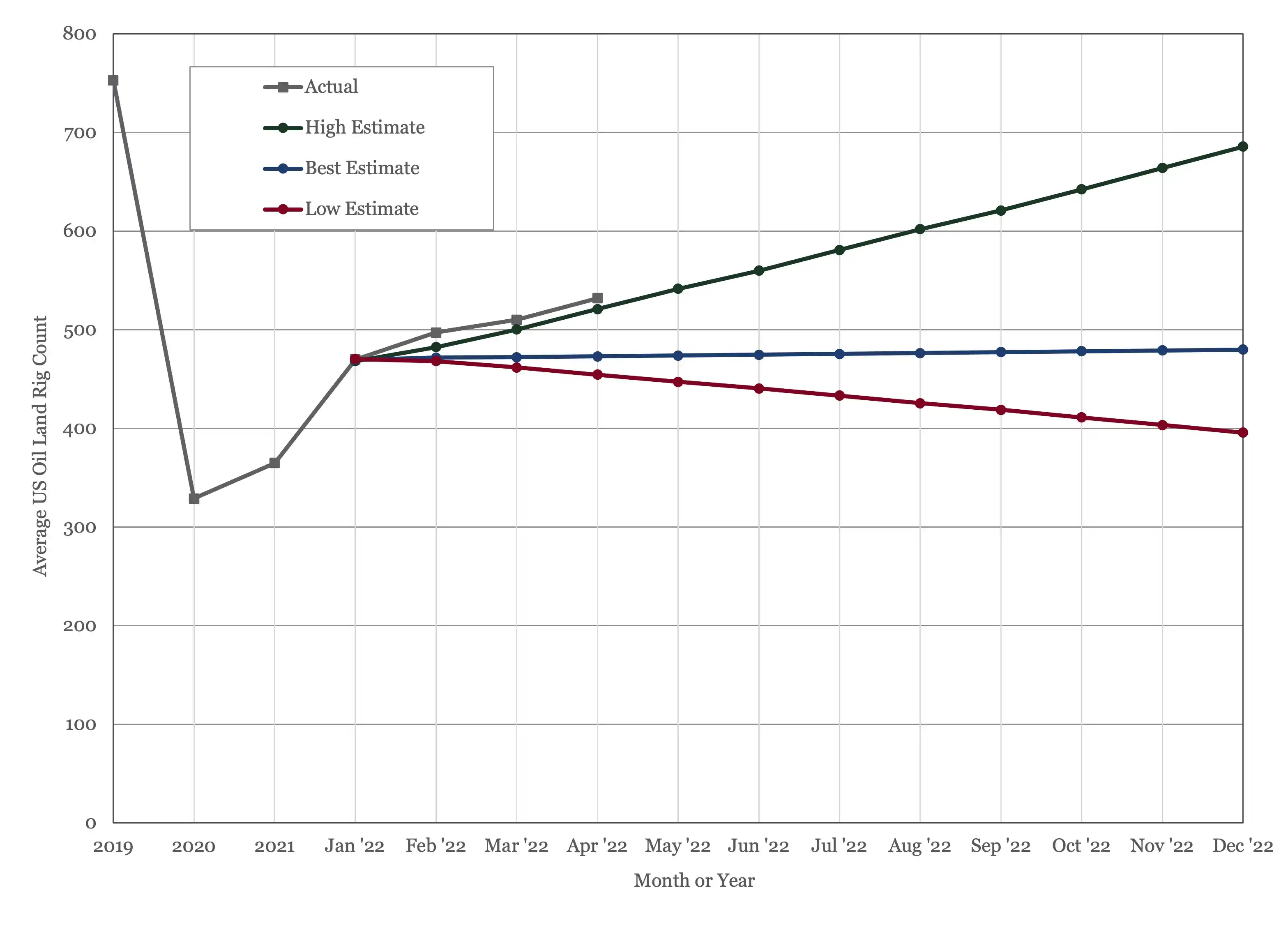

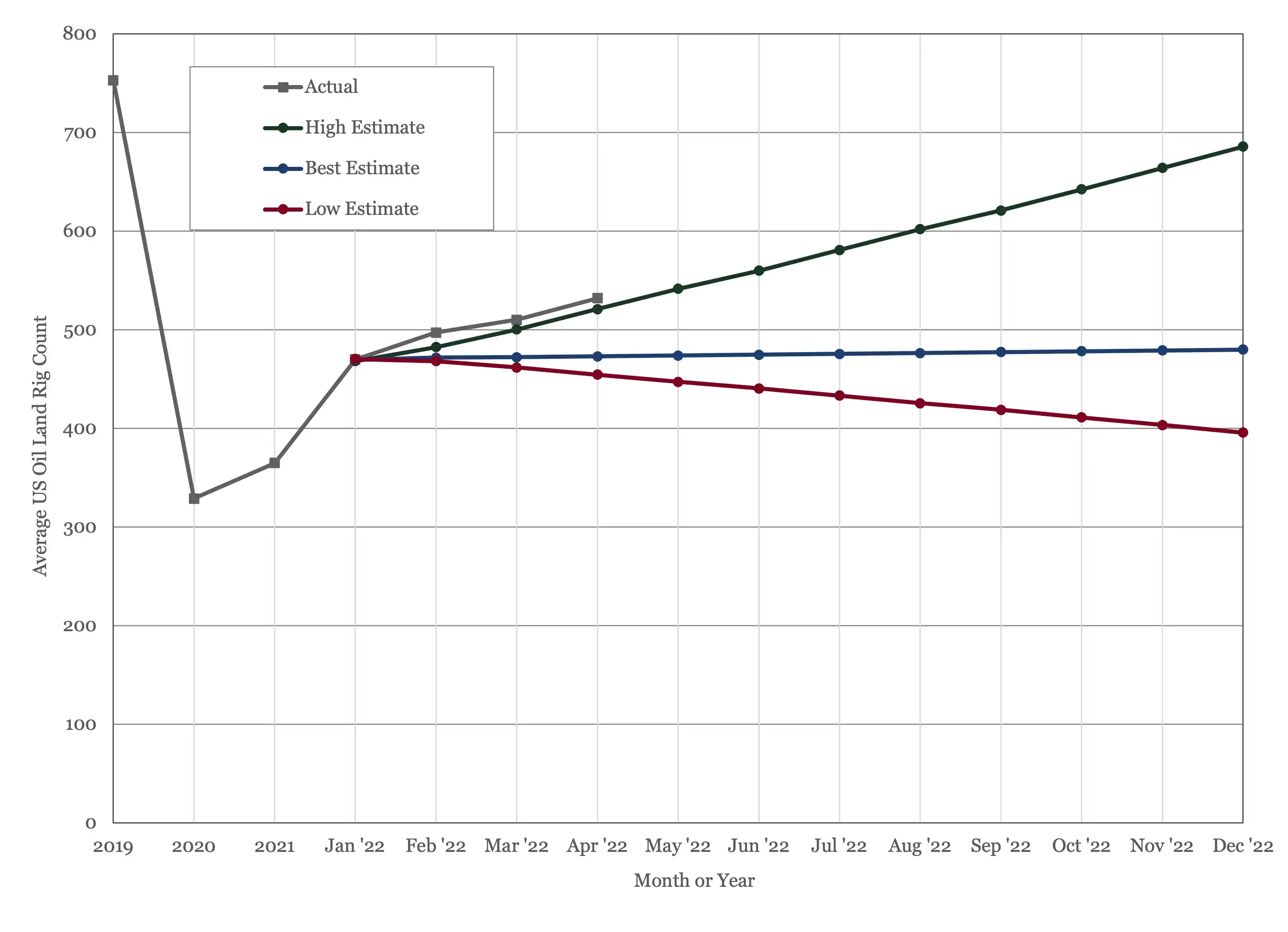

The US land oil rig count continues to rise, hitting 545 on the 13th of May. It is currently tracking slightly above our most aggressive forecast, see Figure 5.

Figure 5 - US Land Oil Rig Count

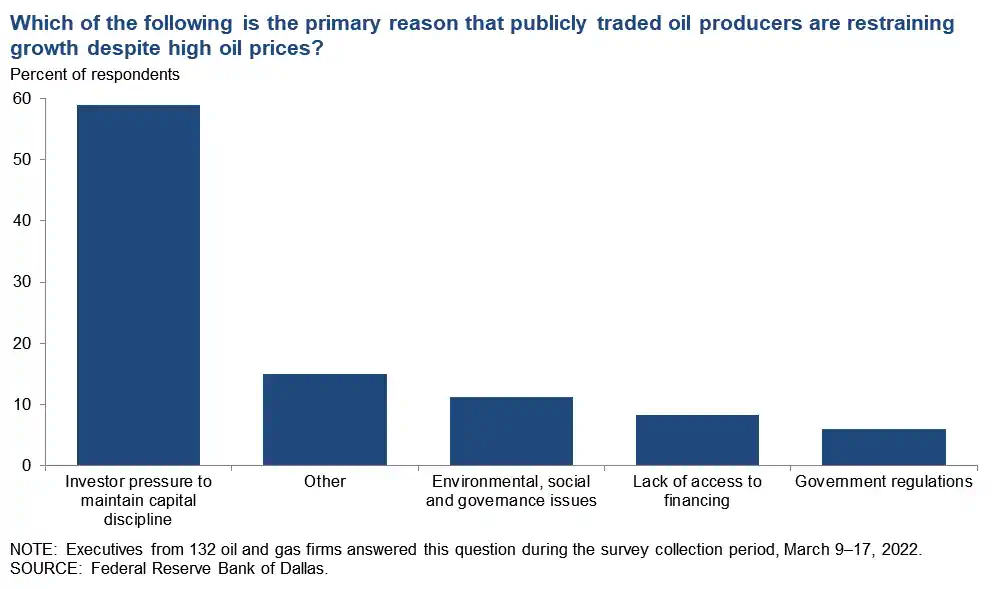

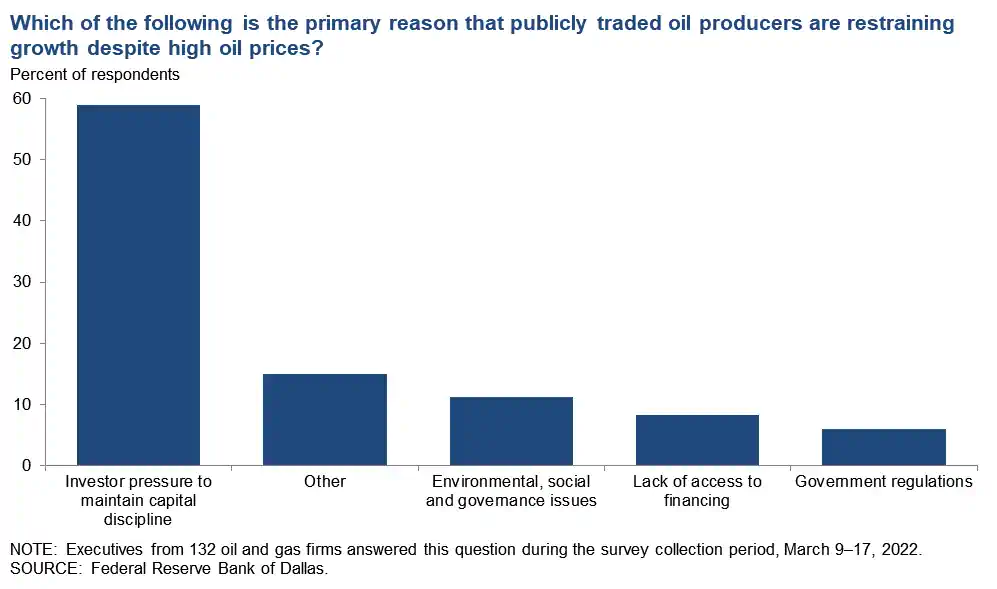

Activity is still not hitting levels the levels that would be expected given current oil prices. As we have discussed in previous editions of this Oil Market Forecast, there are a number of reasons for this – shortages of equipment and manpower, regulatory hurdles, a lack of inventory and capital discipline. Based on recent survey results by the Dallas Federal Reserve (15), see Figure 6, the predominant reason is investor pressure to maintain capital discipline. The survey notes that for those who answered “other” the primary reasons were personnel shortages, equipment shortages and supply-chain issues.

Figure 6 - Survey Results from the Dallas Federal Reserve

Over the long term, regulation may start to play a larger role in limiting US production. Last month the Interior Department offered a smaller than expected number of onshore leases at an increased royalty rate. The month the Interior Department cancelled two US Gulf of Mexico lease sales and one in Alaska, all of which were planned for this year (16). The Department of the Interior cited “lack of industry interest in leasing in the area” as the reason for cancelling the Alaskan lease sale, and “conflicting court rulings that impacted work on these proposed lease sales” for canceling those in the Gulf of Mexico. This is significant as it marks the end of the 2017 – 2022 OCS leasing program. The Interior Department is due to issue a new five-year leasing program in June, but all indications to date are that this will not be ready. This raises the prospect of the OCS going for multiple years without new lease sales.

Both Alaska and the Gulf of Mexico are home to conventional oil and gas resources, and so timelines from leasing new acreage to first oil are in the order or ten to twenty years, meaning that the cancellation of these lease sales will have no impact on the current tightness in domestic supply. Given the timelines, conventional developments in particular require regulatory stability, and without a pipeline of new acreage, exploration and development capability will atrophy. President Biden ran on a commitment to stop drilling on Federal Lands. He has not succeeded in this, but notwithstanding last month’s very limited and deliberately less attractive offering, he seems to have succeeded in preventing new leasing on Federal Lands.

(1) Oil Market Report – May 12th, 2022, IEA, Paris.

(2) Short Term Energy Outlook (STEO), May 5th, 2022, U.S. Energy Information Administration.

(3) “OPEC Monthly Oil Market Report”, Organization of the Petroleum Exporting Countries, May 12th, 2022.

(4) “EU considers shelving ban on Russian oil as Hungary blocks sanctions”, Jacopo Barigazzi, Barbara Moens and Leonie Kijewski, Politico, May 12th, 2022.

(5) “Global growth is slowing, but not stopping - yet”, The Economist, May 15th, 2022

(6) “Oil tumbles about 6% as China COVID lockdowns weigh”, Stephanie Kelly, Reuters, May 9th, 2022

(7) “Tesla’s profits jumped in the first quarter, but challenges loom”, Jack Ewing, The Wall Street Journal, April 20th, 2022

(8) “Oil Trade Group Drafts Carbon-Tax Proposal That Could Raise Prices at the Pump”, Timothy Puko and Ted Mann, The Wall Street Journal, April 21st, 2022.

(9) “19th OPEC and non-OPEC Ministerial Meeting concludes”, OPEC, 18th July 2021

(10) “Russia Tried to Sell a Huge Slug of Oil. Nobody Wanted It”, Joe Wallace and Anna Hirtenstein, The Wall Street Journal, April 26th, 2022

(11) “Russia Says It Is Limiting Oil Data Access To Protect Local Market”, Reuters, April 19th, 2022

(12) “The new ESG realpolitik and the fossil fuel bonanza”, Patrick Jenkins, Financial Times, May 15th, 2022.

(13) “Pumped Dry: Africa’s fuel market”, The Economist, May 7th, 2022.

(14) “European Union Prepares to Ban Russian Oil”, Ben Cahill, Center for Strategic and International Studies, May 10th, 2022.

(15) “Dallas Fed Energy Survey”, Federal Reserve Bank of Dallas, March 23rd, 2022

(16) “Interior Department Abandons Three Lease Sales in Alaska and Gulf of Mexico”, Baker Botts, 12th May 2022

Oil Market Forecast - May 2022

Summary

This month sees some further downgrades in oil demand estimates for the year and continued uncertainty on the impact of the Russian invasion of Ukraine on global supply. The market looks to be in deficit through the forecast period and the surplus of stored crude that was built up over the last couple of years has now been worked off. There are early signs of physical shortages of oil products in some parts of the world, while crude oil prices have retreated from last month’s highs. The US rig count continues its steady climb while the US Interior Department canceled a number of lease sales planned for this year.

A few key points:

- The EIA and OPEC cut their 2022 demand estimates again this month, while the IEA held theirs steady which leaves the range of estimates for the year between 99.4 MMbbl/day and 100.3 MMbbl/day.

- European Union efforts to impose an import ban on Russian oil appear to have stalled in the face of opposition from Hungary and Slovakia

- API members are split over a proposal to lobby US Congress to adopt a carbon tax.

- OPEC+ raises their production target for June by 432,000 bbl/day.

- The oil market is undersupplied through the forecast period, with a supply deficit of 1 – 2 MMbbl/day this year.

- Shortages of diesel, gasoline and jet fuel have been reported across sub-Saharan Africa.

- Spot and futures prices eased back from last month’s highs, but remain above $100/bbl.

- The US oil land rig count rose from 535 last month to hit 545 on May 13th.

- More than half of US publicly listed oil company executives identified capital discipline as the primary reason they were restraining production growth.

- The Interior Department cancelled two lease sales in the Gulf of Mexico and one in Alaska.

Oil Supply and Demand

The IEA held their 2022 oil demand estimate steady at 99.4 MMbbl/day (1). OPEC cut their 2022 demand forecast by 200,000 bbl/day, from 100.5 MMbbl/day last month to 100.3 MMbbl/day this month (2), citing a slowdown in global growth and the impact of a COVID-19 outbreak in China. The EIA cut their 2022 demand estimate the same amount, from 99.8 MMbbl/day to 99.6 MMbbl/day, again citing concerns about growth in China (3). The EIA also cut their 2023 demand estimate by the same margin, bringing that down to 101.5 MMbbl/day.

This month saw news that could impact oil demand over the short, medium, and long term. Dealing with the short term first, the European Union (EU) has been moving towards a ban on the import of Russian oil and oil products as part of their sixth sanctions package in response to the Russian invasion of Ukraine. At the time or writing, it was not clear whether this would move forward (4), as Hungary and Slovakia remain resistant to any import ban. As landlocked nations, Hungary and Slovakia rely on pipelines to deliver oil from Russia, making it much more difficult to source alternate supplies.

An EU ban would have a significant impact on both the oil markets and the Russian economy. The EU imports 3.1 MMbbl/day of crude and Natural Gas Liquids and 1.5 MMbbl/day of oil products from Russia. Some of those volumes will have been impacted by formal sanctions, and the reluctance of some trading companies to deal in Russian crude. Still, an import ban, even the kind of phased import ban that the EU is discussing, would result in some shut in production, at least for a period while Russia re-oriented its exports. Russia is also being forced to sell those re-oriented exports at a sharp discount - $30/bbl is the widely quoted figure – so even if Russian export levels eventually recovered, revenues would suffer.

Both the EIA and OPEC cited the COVID-19 outbreak in China as a basis to downgrade their demand estimates. Nomura reported this week that 41 cities, account for 30% of China’s GDP were in full or partial lockdown (5). Reuters reported that Chinese crude oil imports were down by 4.8% in the first four months of 2022, compared to the prior year (6), although imports did climb in April.

In the medium term, an already tight oil market, exacerbated by the Russian invasion, has driven oil prices above $100/bbl at exactly the same time as mainstream auto manufacturers begin to roll out their electric vehicle line ups. High oil prices should provide a tailwind to electric vehicle sales as consumers in the market for a new vehicle look for ways to insulate themselves from rising fuel costs. Rising electric vehicle sales will, in turn, provide a headwind to rising global oil demand. As Tesla recently reported (7), however, oil is not the only commodity that has seen recent inflation. Tesla highlighted the soaring cost of lithium as the reason they have had to raise their prices. While higher prices have had no impact on Tesla’s sales figures, other electric vehicle manufacturers may face more of a struggle to convince the public to go electric.

Looking at longer term trends, The Wall Street Journal (8) reported that the American Petroleum Institute (API) membership has split over an API proposal to implement a carbon tax. The draft proposal, yet to be approved by the API’s executive committee, would urge Congress to impose a carbon tax of $35/ton to $50/ton. The measure is supported by some European members such as Shell and Equinor but opposed by a number of US refiners and Independents.

The author’s own opinion is that a carbon tax is the most efficient way to limit carbon dioxide emissions – it places a price on the thing that causes the problem and lets the market, rather than politicians, resolve it. The author is also coming around to the view that a carbon tax is politically impossible in the US, as the electorate is simply too sensitive to gasoline prices. The opposition to the API’s initiative appears to stem from a combination of doubt that it would ever be passed, together with the recognition that it would alienate political allies. The Republican Party will attempt to paint the Biden administration’s policies as responsible for energy price inflation in this year’s mid-term elections. Having to explain away a policy proposal from the industry that would push them up even further would be a huge electoral liability. Neither will the proposal win the API any friends among the Democrats, whose climate change policies are more focused on incentivizing a transition to alternatives rather than taxing carbon.

On the supply side, OPEC+ stuck to their guns and raised their output target for June by 432,000 bbl/day, which takes total target OPEC+ production to 42,558 MMbbl/day. Going back to the 19th OPEC and Non-OPEC Ministerial Meeting of July 18th, 2021 (9), reference OPEC+ production levels for May 2022 were 45,485 MMbbl/day. Not only is the current OPEC+ target nearly 3 MMbbl/day short of their reference production level, as reported over the last few months OPEC+ is struggling to achieve even that, lower, target. The IEA did not publish April figures in their May Oil Market Report, but in March OPEC+ production was 1.63 MMbbl/day below target.

The Russian oil industry is struggling to adjust to formal and informal sanctions on exports of Russian oil. In late April Rosneft tried and failed to auction close to 38 MMbbl of oil (10). Rosneft was forced to run the sale itself as the trading companies it normally relies upon were unwilling to handle the sale. The exact impact on production will soon become more difficult to gauge as Russia’s Energy Ministry has announced that it will limit access to statistics on Russian oil production and exports (11). The intent may be to make Russian oil harder to track, making it easier to evade sanctions. The Wall Street Journal reported a spike in Russian crude oil exports to ‘destination unknown’ in April. This designation is often used by sanctioned countries such as Iran and Venezuela to disguise the origin of their oil.

In the medium term, there does appear to be, if not a renewed embrace of fossil fuels, then perhaps a more positive tone from investors. Last week Blackrock announced that it wouldn’t be able to support as many pro-climate environmental or social proposals as it had in the past, arguing that these were becoming increasingly prescriptive and constraining (12). This change of posture may signal a growing willingness to invest in the oil & gas industry.

Overall, the impact of formal and informal sanctions appears to be less severe that had been predicted last month. In their latest Oil Market Report, the IEA think that production was down by 1 MMbbl/day in April, rather than the 1.5 MMbbl/day that they had estimated the month before. The drop in May is likely to be sharper, as the sanctions that were announced in March did not come into full effect until the 22nd of April. The net effect is that the oil market remains in a deficit through the rest of the forecast period, as shown in Figure 1.

Figure 1 - Supply and Demand Surplus Forecast

Oil Storage

Global oil inventory drawdowns for 2022 are down from last month’s estimates, on higher forecast US production, at 488 MMbbl. This is still below the overall build of 1,072 MMbbl in 2020 but combined with stock draws of 321 MMbbl last year we are below the 5-year average now and stocks will fall below 2019 levels by year end. The EIA estimates that OECD inventories are 315 MMbbl below their 5-year average.

Figure 2 - Global Storage Chart

While OECD stocks are running low, across sub–Saharan Africa, there are real fuel shortages. Last week the Economist reported physical shortages of jet fuel, gasoline and diesel in Senegal, South Africa, Cameroon, Kenya, and Nigeria (13). The physical shortages have reached Africa first due to a combination of factors. The current backwardation in the Brent futures market is driving traders to sell crude immediately into Asian markets, rather than use floating storage offshore west Africa, where local traders can pick up small volumes as those tankers pass by. Hedging costs for local traders are increasing in line with the oil price, forcing those unable to expand their balance sheets to reduce imports. Africa has little domestic refining capacity, which is why people are forced to queue for fuel in Nigeria, a major crude oil exporter, and most countries in sub-Saharan Africa do not maintain supplies in reserve, as is common in the OECD. Maintaining a strategic reserve does not eliminate the risk of shortages, it just delays them. The longer the current production deficit persists, the more nations will start to see this type of supply shortage.

Oil Prices

Both Brent and WTI spot and futures prices were down this month, but $100/bbl appears to be a floor. The EIA raised their estimate for 2023 prices by $5/bbl to $97/bbl. The Center for Strategic and International Studies warned that EU sanctions on Russian oil would be likely to push prices sharply higher again (14).

Figure 3 - Brent Crude Oil Futures

Figure 4 - WTI Crude Oil Futures

US Activity

The US land oil rig count continues to rise, hitting 545 on the 13th of May. It is currently tracking slightly above our most aggressive forecast, see Figure 5.

Figure 5 - US Land Oil Rig Count

Activity is still not hitting levels the levels that would be expected given current oil prices. As we have discussed in previous editions of this Oil Market Forecast, there are a number of reasons for this – shortages of equipment and manpower, regulatory hurdles, a lack of inventory and capital discipline. Based on recent survey results by the Dallas Federal Reserve (15), see Figure 6, the predominant reason is investor pressure to maintain capital discipline. The survey notes that for those who answered “other” the primary reasons were personnel shortages, equipment shortages and supply-chain issues.

Figure 6 - Survey Results from the Dallas Federal Reserve

Over the long term, regulation may start to play a larger role in limiting US production. Last month the Interior Department offered a smaller than expected number of onshore leases at an increased royalty rate. The month the Interior Department cancelled two US Gulf of Mexico lease sales and one in Alaska, all of which were planned for this year (16). The Department of the Interior cited “lack of industry interest in leasing in the area” as the reason for cancelling the Alaskan lease sale, and “conflicting court rulings that impacted work on these proposed lease sales” for canceling those in the Gulf of Mexico. This is significant as it marks the end of the 2017 – 2022 OCS leasing program. The Interior Department is due to issue a new five-year leasing program in June, but all indications to date are that this will not be ready. This raises the prospect of the OCS going for multiple years without new lease sales.

Both Alaska and the Gulf of Mexico are home to conventional oil and gas resources, and so timelines from leasing new acreage to first oil are in the order or ten to twenty years, meaning that the cancellation of these lease sales will have no impact on the current tightness in domestic supply. Given the timelines, conventional developments in particular require regulatory stability, and without a pipeline of new acreage, exploration and development capability will atrophy. President Biden ran on a commitment to stop drilling on Federal Lands. He has not succeeded in this, but notwithstanding last month’s very limited and deliberately less attractive offering, he seems to have succeeded in preventing new leasing on Federal Lands.

(1) Oil Market Report – May 12th, 2022, IEA, Paris.

(2) Short Term Energy Outlook (STEO), May 5th, 2022, U.S. Energy Information Administration.

(3) “OPEC Monthly Oil Market Report”, Organization of the Petroleum Exporting Countries, May 12th, 2022.

(4) “EU considers shelving ban on Russian oil as Hungary blocks sanctions”, Jacopo Barigazzi, Barbara Moens and Leonie Kijewski, Politico, May 12th, 2022.

(5) “Global growth is slowing, but not stopping - yet”, The Economist, May 15th, 2022

(6) “Oil tumbles about 6% as China COVID lockdowns weigh”, Stephanie Kelly, Reuters, May 9th, 2022

(7) “Tesla’s profits jumped in the first quarter, but challenges loom”, Jack Ewing, The Wall Street Journal, April 20th, 2022

(8) “Oil Trade Group Drafts Carbon-Tax Proposal That Could Raise Prices at the Pump”, Timothy Puko and Ted Mann, The Wall Street Journal, April 21st, 2022.

(9) “19th OPEC and non-OPEC Ministerial Meeting concludes”, OPEC, 18th July 2021

(10) “Russia Tried to Sell a Huge Slug of Oil. Nobody Wanted It”, Joe Wallace and Anna Hirtenstein, The Wall Street Journal, April 26th, 2022

(11) “Russia Says It Is Limiting Oil Data Access To Protect Local Market”, Reuters, April 19th, 2022

(12) “The new ESG realpolitik and the fossil fuel bonanza”, Patrick Jenkins, Financial Times, May 15th, 2022.

(13) “Pumped Dry: Africa’s fuel market”, The Economist, May 7th, 2022.

(14) “European Union Prepares to Ban Russian Oil”, Ben Cahill, Center for Strategic and International Studies, May 10th, 2022.

(15) “Dallas Fed Energy Survey”, Federal Reserve Bank of Dallas, March 23rd, 2022

(16) “Interior Department Abandons Three Lease Sales in Alaska and Gulf of Mexico”, Baker Botts, 12th May 2022

Explore Our Services

Business Development

Oil & Gas an extractive industry, participants must continuously find and develop new oil & gas fields as existing fields decline, making business development a continuous process.

Strategy

We approach strategy through a scenario driven assessment of the client’s current portfolio, organizational competencies, and financial framework. The strategy defines portfolio actions and coveted asset attributes.

Origination

Deal origination consists of identifying coveted assets, assets with attributes consistent with the client’s strategy, and qualified buyers. We advocate a proactive approach to business development and will undertake outreach on our client’s behalf.

Transaction Support

Transaction support consists of in depth asset evaluation, negotiation of commercial agreements or preparation of license round submission and close out of conditions. We can also aid in joint venture set up and management and asset maturation as required.