Oil Market Forecast - December 2021

Summary

Another turbulent month, and not for the reasons expected. While Omicron made the headlines and immediate impact on prices, the more significant news this month may be a shift in sentiment on supply and demand balance next year, driven by resurgent supply. We spend some time this month looking at supply and demand, and as US production moves back to center stage, US investment next year.

A few key points:

- The IEA made a small demand downgrade to account for Omicron, the EIA made a more significant adjustment and OPEC held their demand estimates flat.

- There was a coordinated release from the US strategic petroleum reserve, but the impact was not significant, certainly when compared to the impact of Omicron on prices.

- OPEC+ raised supply for December in line with their schedule and announced a further 400,000 bbl/day in January.

- The US land oil rig count reached 459.

Oil Supply and Demand

The IEA (1) downgraded their 2021 and 2022 demand estimates by 100,000 bbl/day to reflect what they think will be a limited impact on oil demand from the Omicron variant. This sees demand at 96.4 MMbbl/day and 99.7 MMbbl/day in 2021 and 2022 respectively. The EIA (2) was less sanguine, shaving 500,000 bbl/day off their 2022 demand estimate to bring it down to 100.4 MMbbl/day and signaled that the uncertainty around the path Omicron takes could see further revision over the coming months. This may reflect some revision to historical data as they also lowered their 2021 demand estimate from 97.5 MMbbl/day to 96.9 MMbbl/day month over month. OPEC (3) held their 2021 and 2022 demand estimates steady at 97.7 MMbbl/day and 100.6 MMbbl/day respectively.

On the supply side, the last month saw a release from the US Strategic Petroleum Reserve in co-ordination with several other nations – Japan, China and South Korea. The volumes committed were nominal – 50 MMbbl by the US, which is about 12 hours of global demand – and did little to affect the market. There had been a suggestion that the OPEC+ group of nations would respond by reversing their decision to raise production quotas in December, but in the event that did not happen. At their meeting of the 2nd of December (4), the OPEC+ group of nations agreed that they would maintain their 400,000 bbl/day December increase as planned and add a further 400,000 bbl/day in January 2022.

While OPEC+ is currently holding course with a measured return of production, high oil prices and a return to pre-pandemic quota levels are starting to reveal divergent dynamics within the group. As mentioned last month, Kuwait’s underlying production capacity has declined and both Nigeria and Angola have struggled to reach their pandemic reduced quotas over recent months (5). On the other hand, Russia has indicated that it is ready to return to full production capacity and Iran has announced that it intends to raise its production to its pre-sanction level of 4 MMbbl/day by March 2022 (6). These tensions suggest that maintaining the discipline and unity that has been the hallmark of the OPEC+ meetings for the last 18 months may become increasingly difficult as production levels return to normal in mid 2022.

Recent capital budget announcements by two International Oil Companies (IOC’s) have not indicated a willingness to return to pre-pandemic investment levels (7). In a reversal of its pre-pandemic strategy, Exxon committed to a reduced capital budget of $20 - $25 billion per annum through 2027, while Chevron committed to $15 billion per annum through 2025. This constitutes a 17% - 33% reduction for Exxon and a 25% reduction for Chevron against pre-pandemic levels.

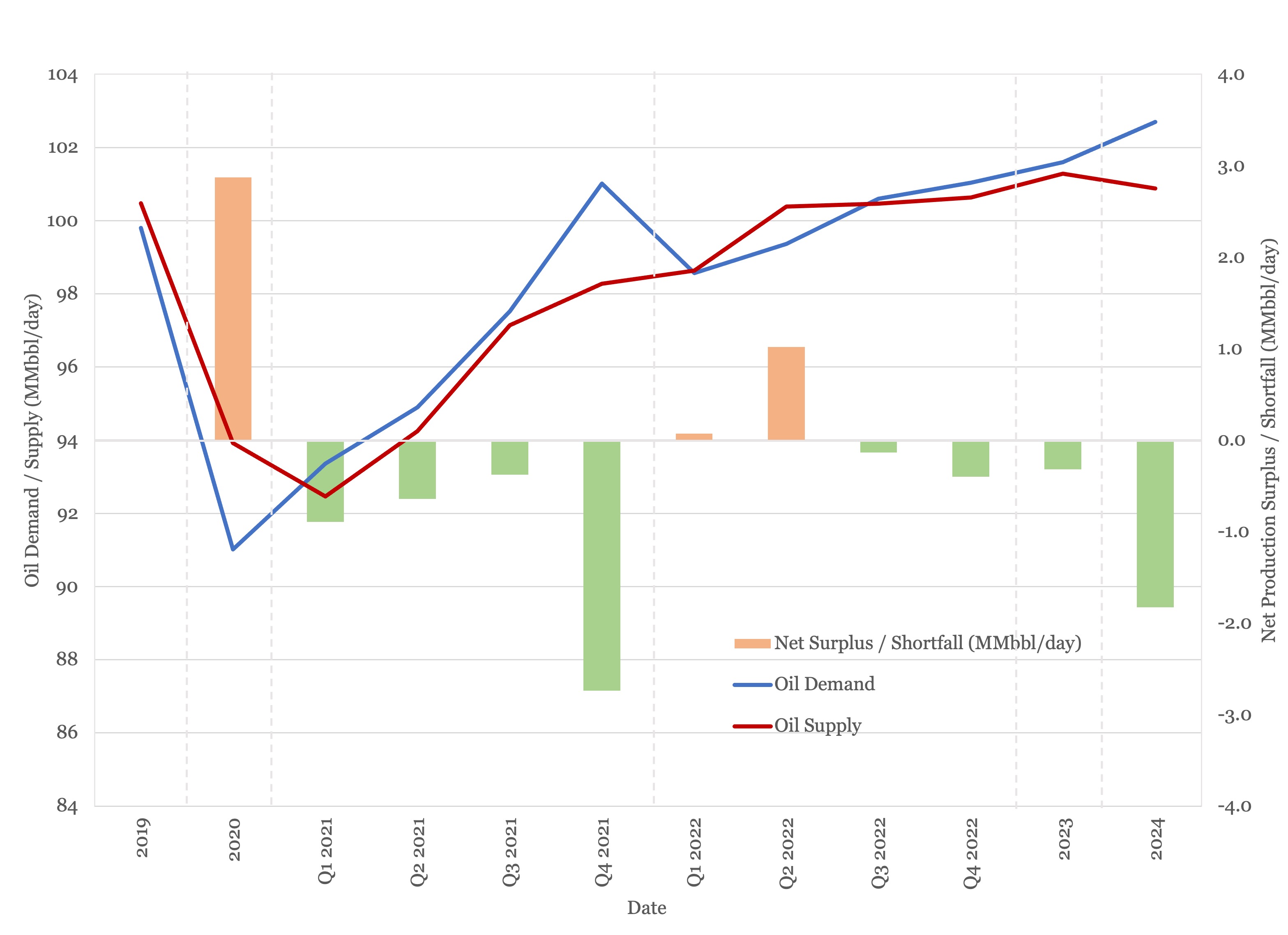

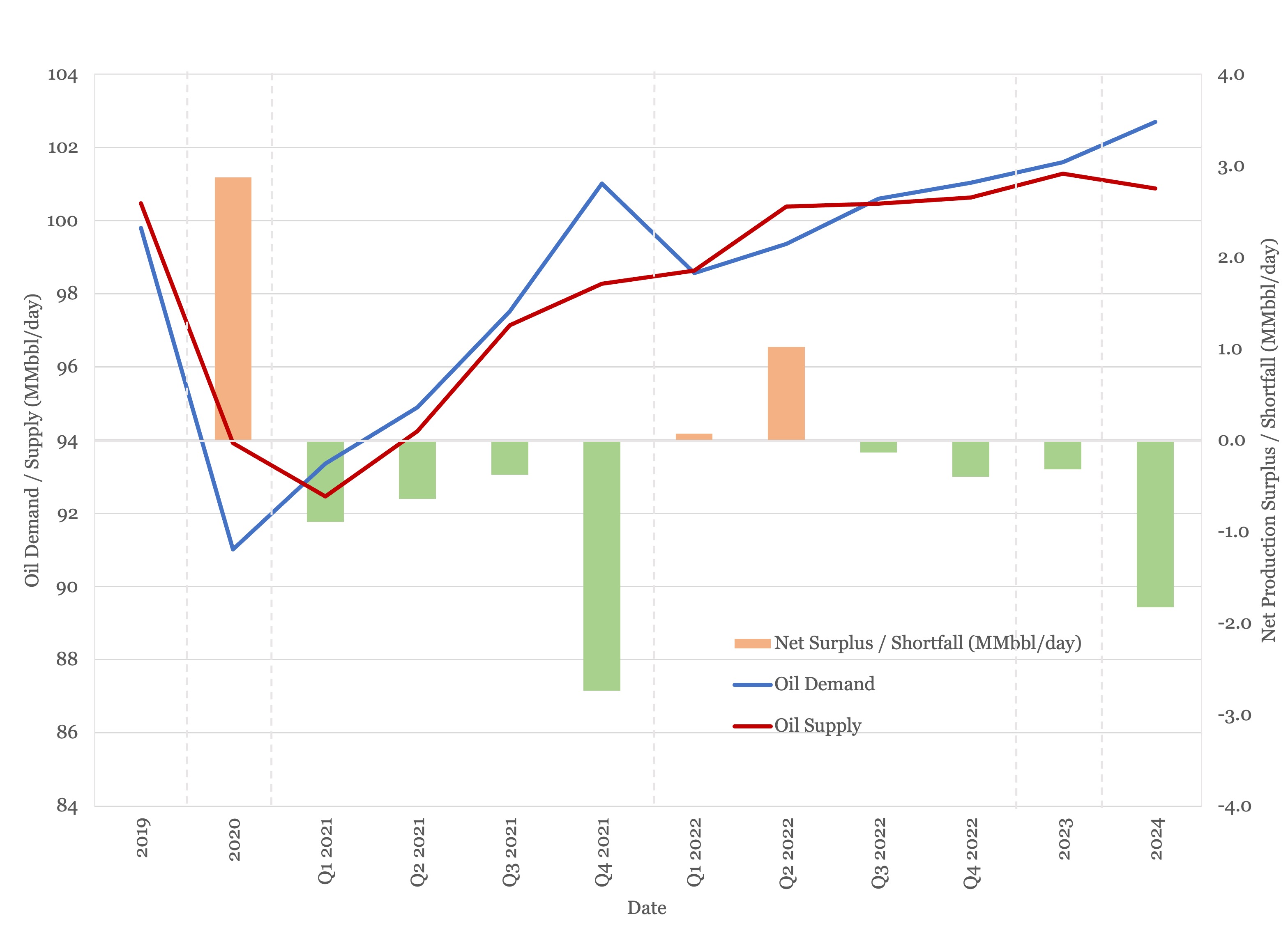

All three agencies are now predicting a supply surplus in 2022, with a return of both OPEC and non-OPEC supply. The IEA predicts that Canada, Brazil, the US, Russia and Saudi Arabia will all hit new production records next year. Our own model shows the market to be in a small surplus for 2022, with a large surplus in the first half of the year largely offset by a deficit in the second half. The major difference between our own forecast and that of the main agencies is in US production; we predict the US will add about 200,000 bbl/day next year whereas all three agencies are predicting much stronger US production growth. Our forecast is shown in Figure 1, below.

Figure 1 - Supply and Demand Surplus Forecast

Oil Storage

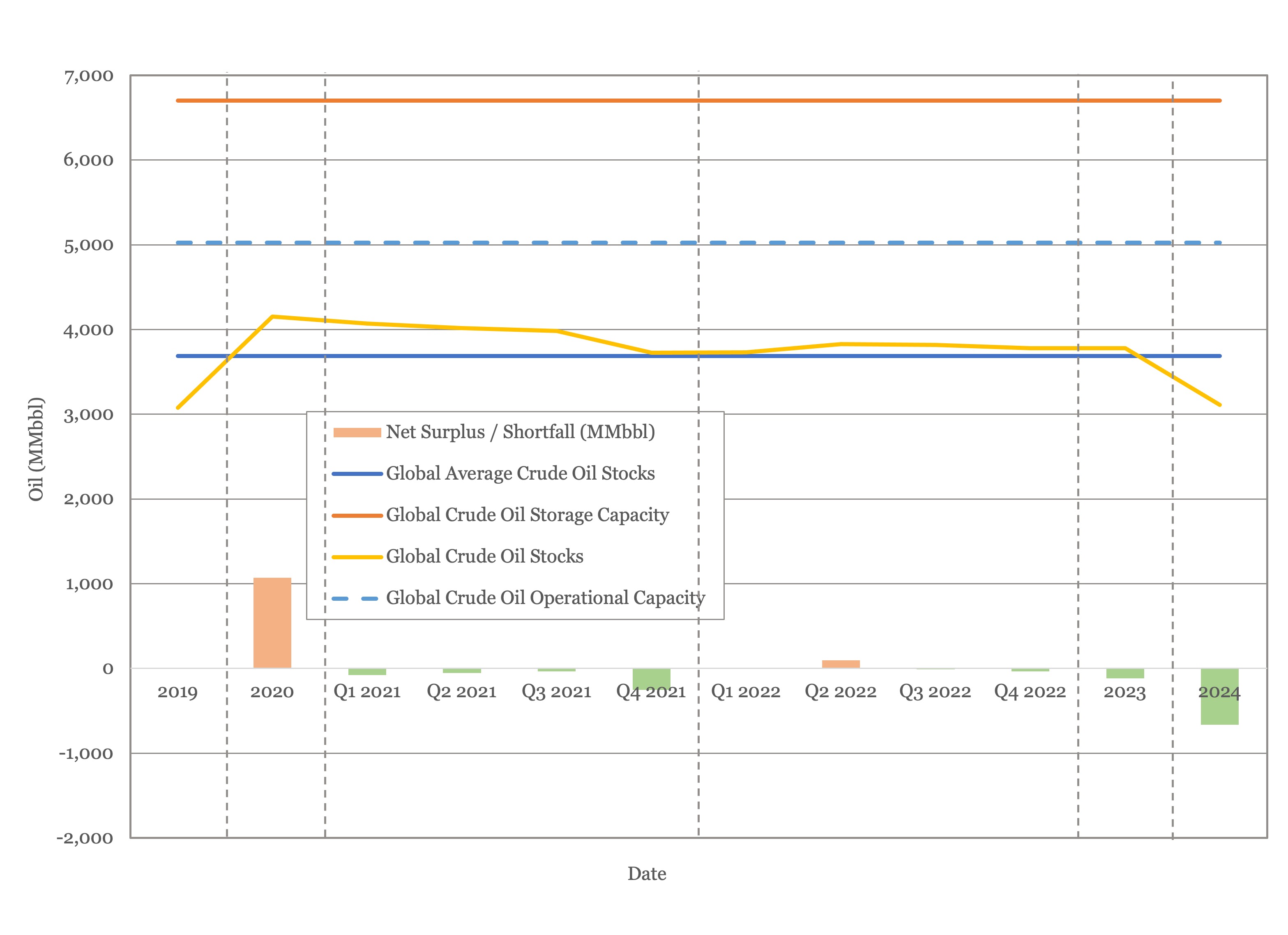

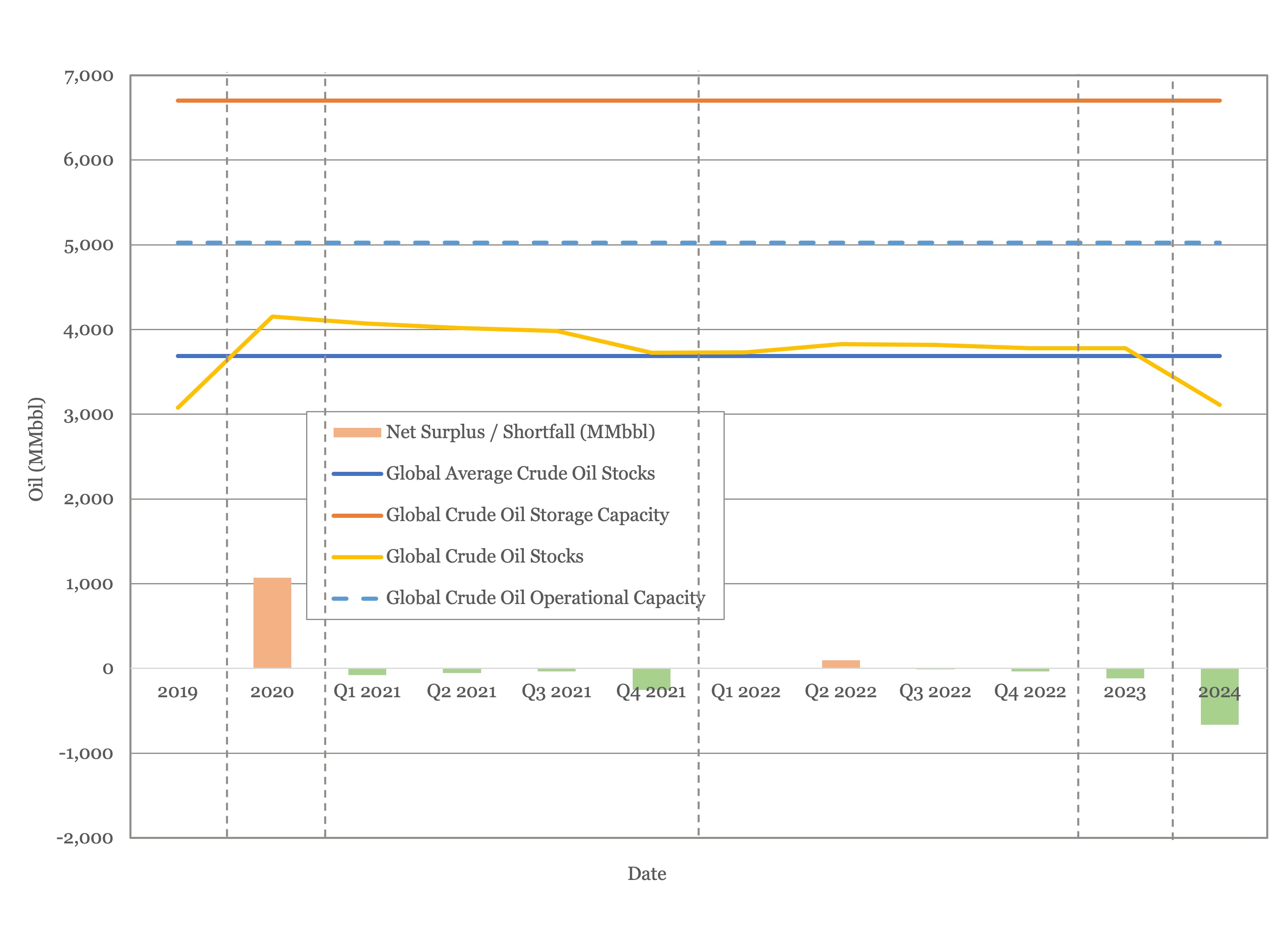

We estimate global oil inventory drawdowns of 322 MMbbl in 2021, flipping to a surplus of 66 MMbbl in 2022 as OPEC+ returns to reference production levels. Figure 2 shows global storage capacity and inventories. If supply and demand follow the current forecast, global inventories will be around the five-year average for the 4th quarter 2021 and remain about that level through 2022 and 2023.

Figure 2 - Global Storage Chart

Oil Prices

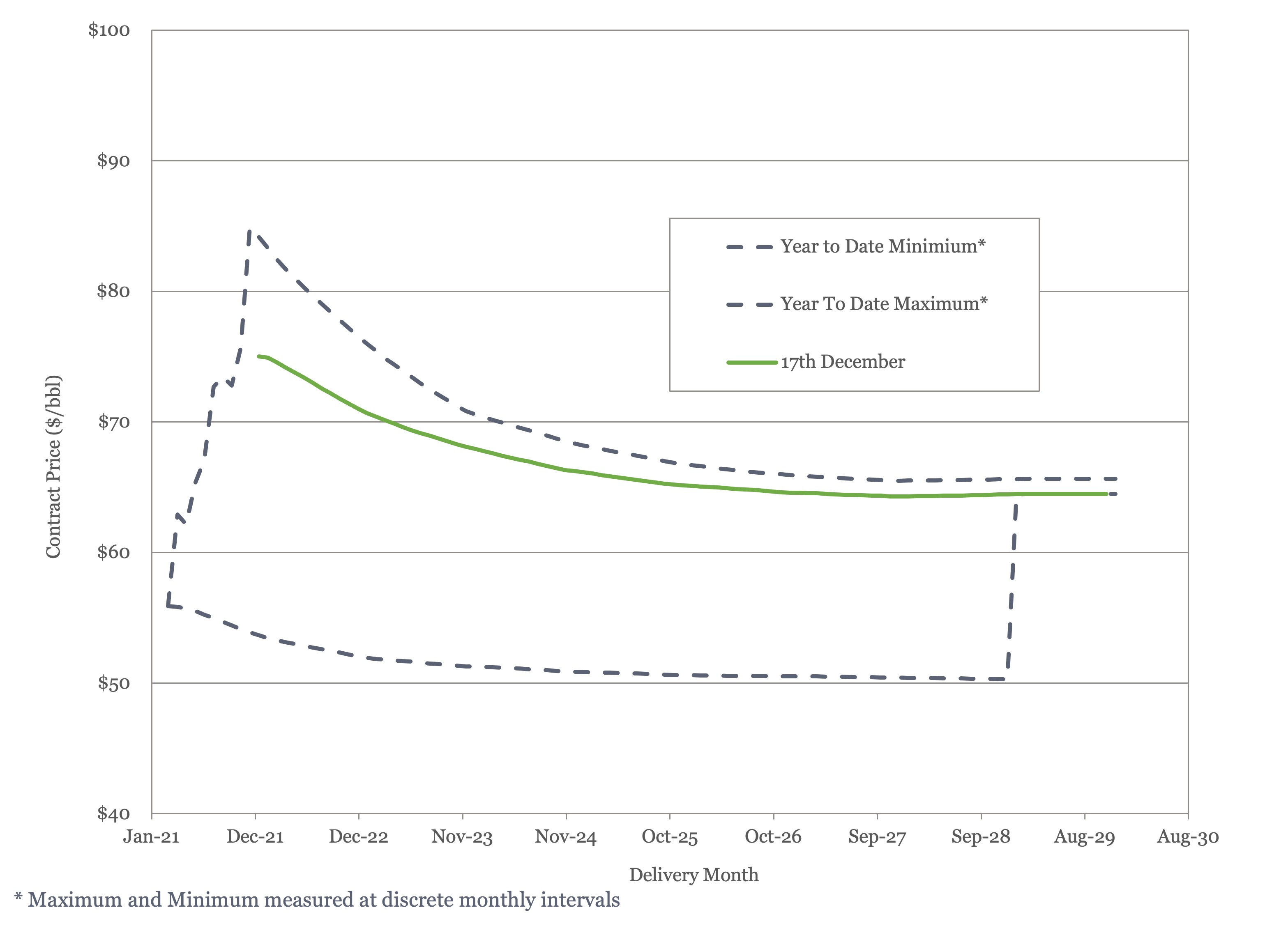

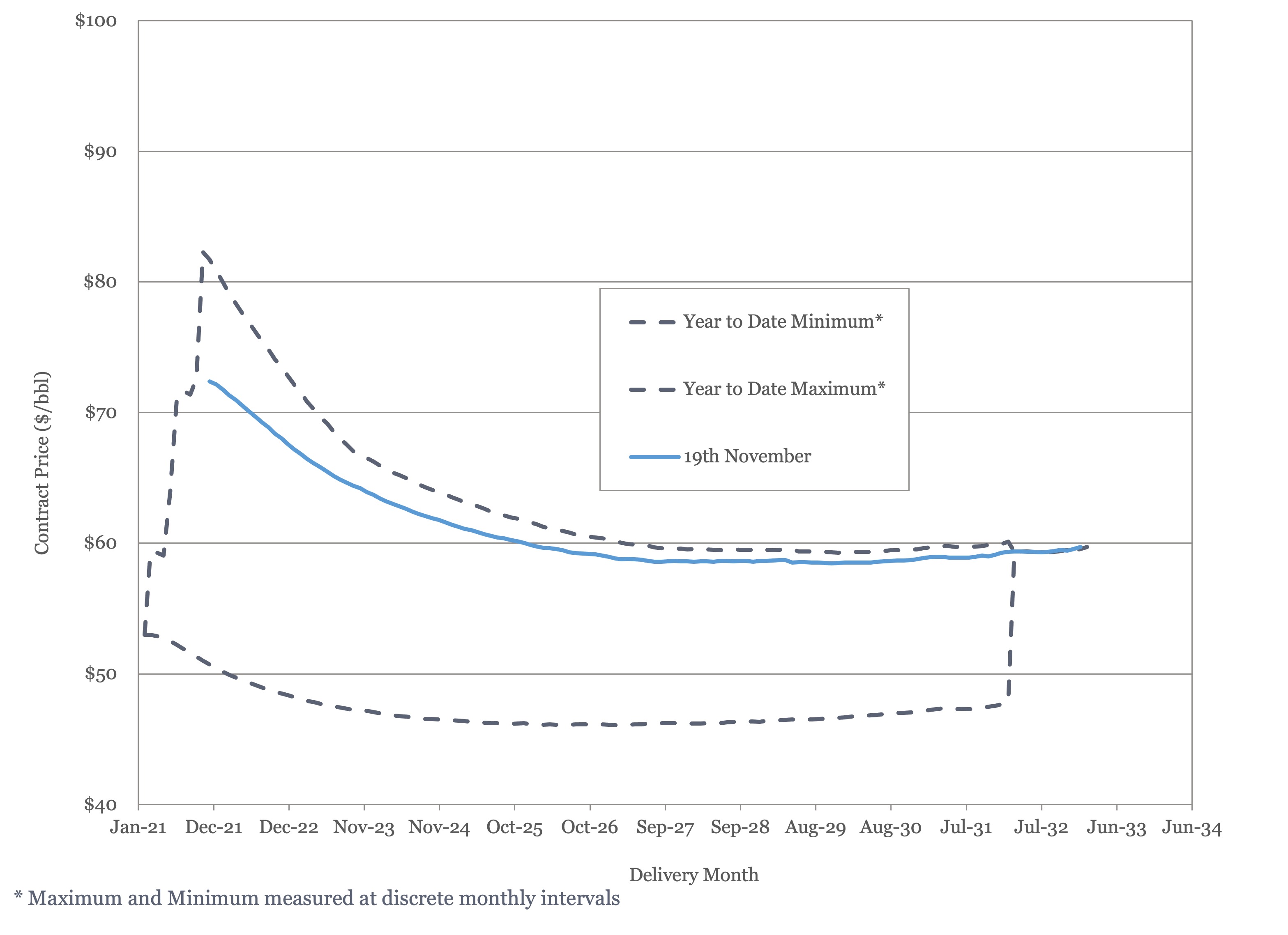

Omicron achieved what a coordinated release of oil from national strategic reserves failed to with oil prices dropping sharply over the last month. WTI fell from near $85/bbl last month to $65/bbl before bouncing back to just above $70/bbl at the time of writing. The EIA is now predicting downward price pressure in 2022, as stocks start to build again. They are forecasting a Brent average price of $73/barrel in Q1 next year falling to $67/bbl by Q4.

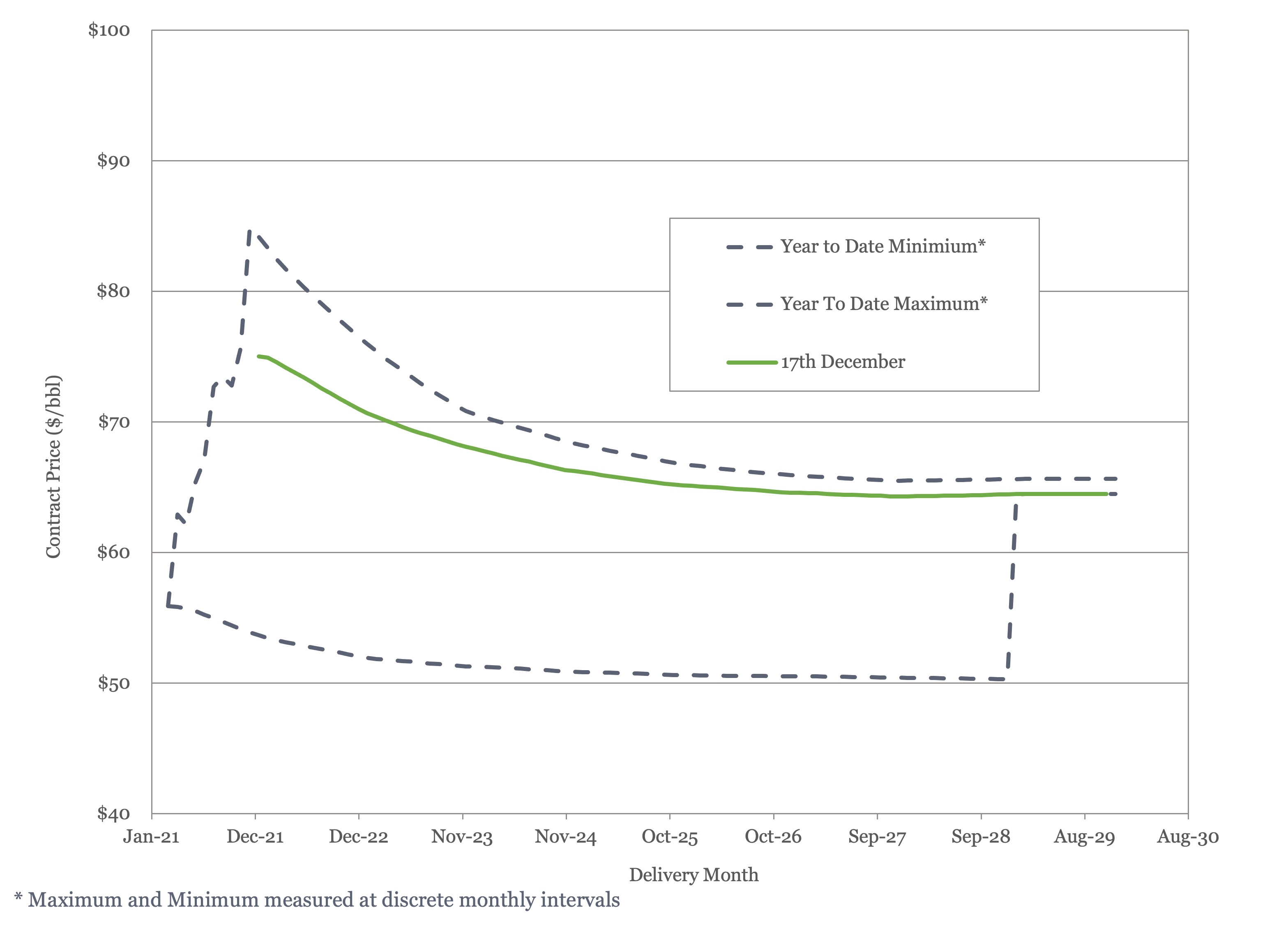

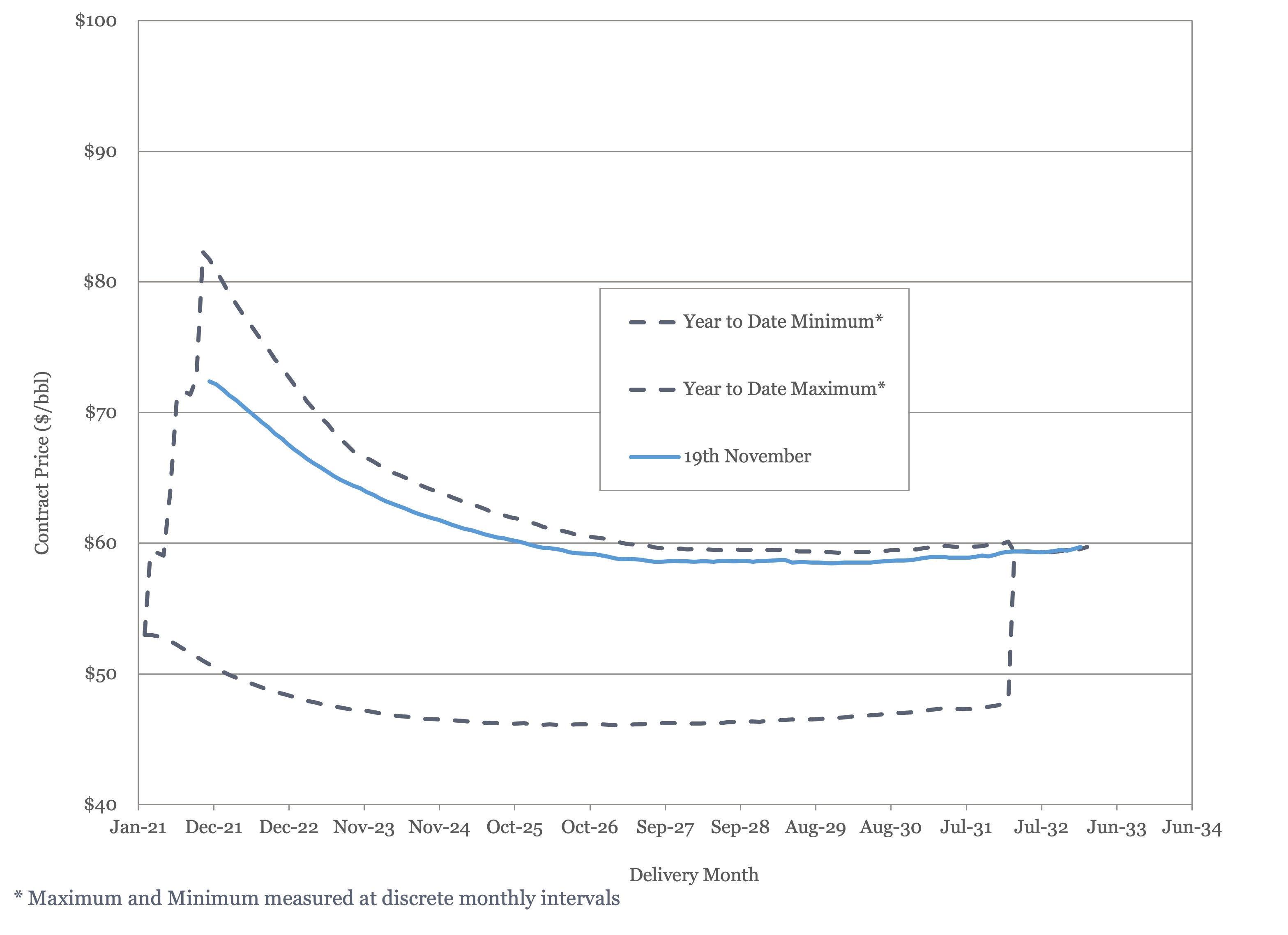

Both Brent and WTI futures fell, with steeper near term falls. Brent remains close to $65/bbl out to the end of the decade, with WTI close to $60/bbl.

Figure 3 - Brent Crude Oil Futures

Figure 4 - WTI Crude Oil Futures

US Activity

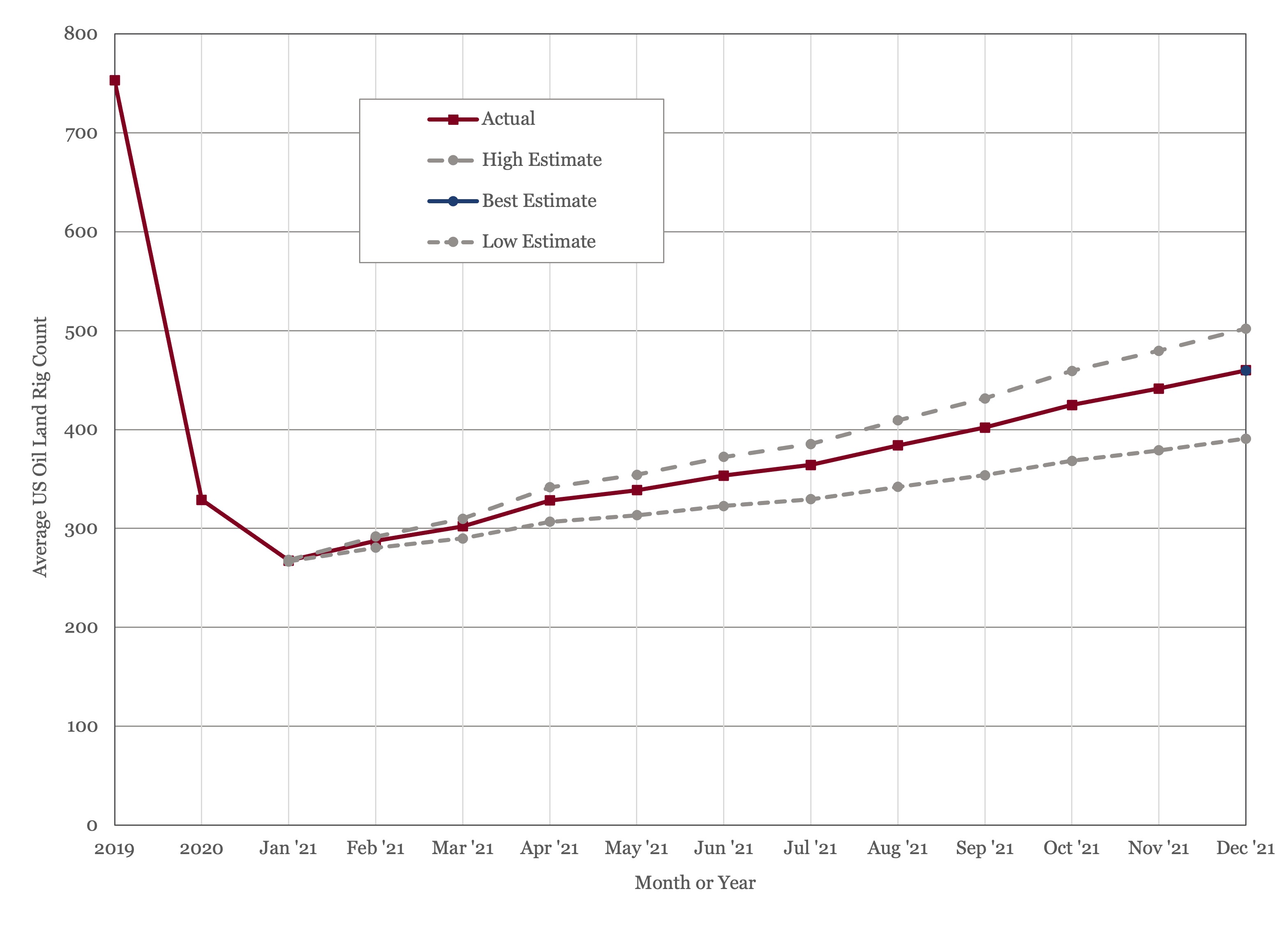

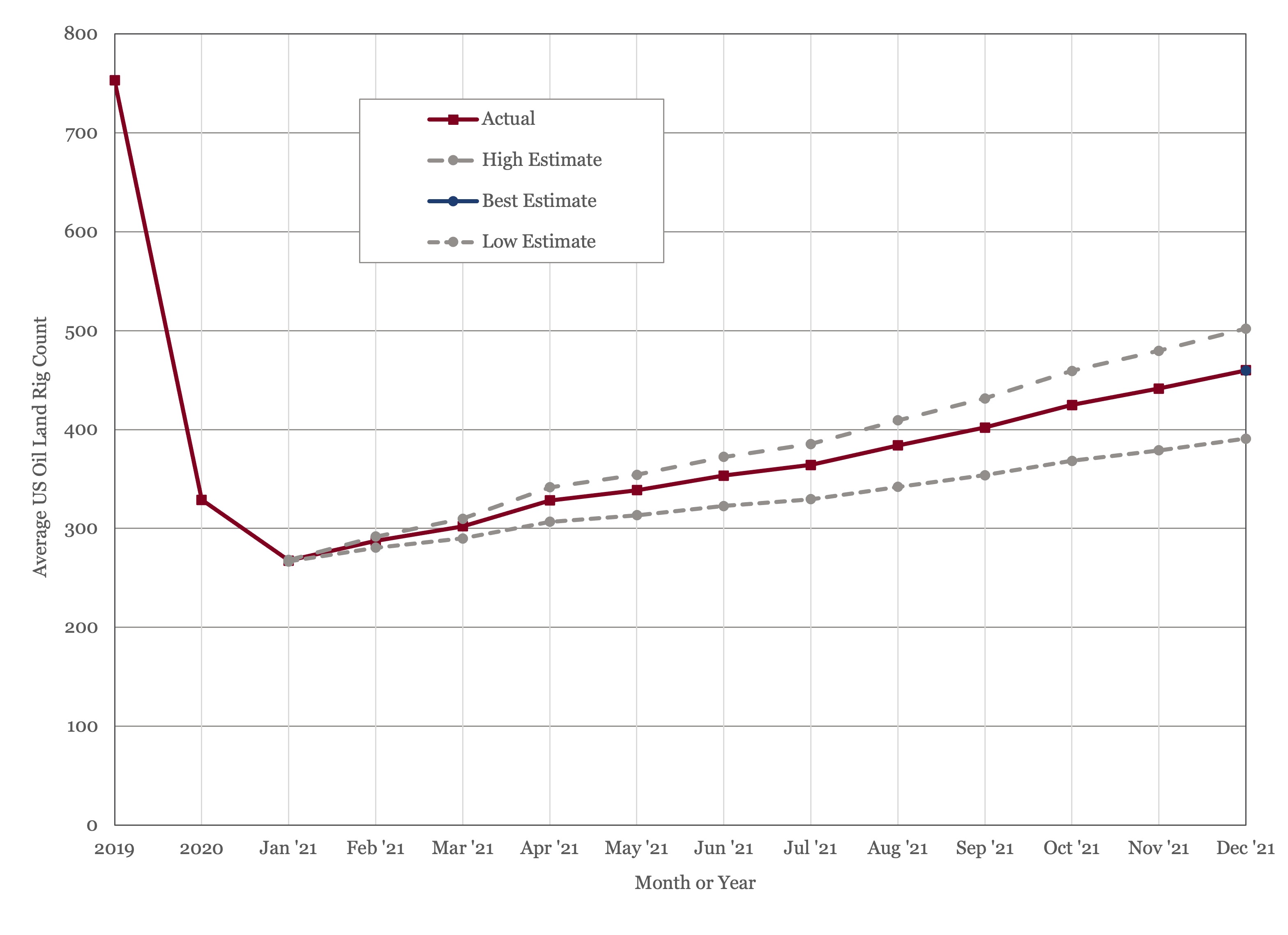

As OPEC+ returns production to normal next year, US production will once more move to center stage in determining oil market balance. The US land oil rig count continued to rise this month, reaching 459 on the 17th of December. We expect it to average 365 for 2021, up slightly from the 321 count of 2020, but still down sharply from the 753 average of 2019.

Figure 5 - US Land Oil Rig Count

We expect US production to average 16.4 MMbbl/day for 2021, down slightly from 2020. Our guestimate is that US onshore capital budgets will rise by about 20% next year in real terms, which would equate to an average rig count of about 440 for the year, around current activity levels. This would be enough to boost production by ~ 200,000 bbl/day to 16.6 MMbbl/day in 2022.

As noted in the Supply and Demand section, the IEA are predicting US production in 2022 will exceed its record 2019 level of 17.2 MMbbl/day. According to our model, to raise average US production in 2022 by 900,000 bbl/day would require an average 2022 oil land rig count of 570, suggesting rig counts at 2019 levels by the end of 2022. That would imply a CAPEX budget increase of 60% year on year, which doesn’t seem consistent with the current philosophy of profits over production.

(1) Oil Market Report – December 2021, International Energy Agency

(2) Short Term Energy Outlook (STEO), December 2nd, 2021, U.S. Energy Information Administration.

(3) “OPEC Monthly Oil Market Report”, Organization of the Petroleum Exporting Countries, November 11th, 2021.

(4) 23rd OPEC and Non-OPEC Ministerial Meeting, December 2nd, 2021.

(5) “Russia Is Ready to Return to Pre-Pandemic Oil Production”, Tsvetana Paraskova, Oilprice.com, November 29th, 2021.

(6) “Iran seeks to return oil output to pre-sanction levels”, Arsalan Shahla, World Oil, November 28th, 2021

(7) “Exxon to Continue Leaner Spending as Covid-19 Threat Lingers”, Christopher Matthews, December 1st, Wall Street Journal.

Oil Market Forecast - December 2021

Summary

Another turbulent month, and not for the reasons expected. While Omicron made the headlines and immediate impact on prices, the more significant news this month may be a shift in sentiment on supply and demand balance next year, driven by resurgent supply. We spend some time this month looking at supply and demand, and as US production moves back to center stage, US investment next year.

A few key points:

- The IEA made a small demand downgrade to account for Omicron, the EIA made a more significant adjustment and OPEC held their demand estimates flat.

- There was a coordinated release from the US strategic petroleum reserve, but the impact was not significant, certainly when compared to the impact of Omicron on prices.

- OPEC+ raised supply for December in line with their schedule and announced a further 400,000 bbl/day in January.

- The US land oil rig count reached 459.

Oil Supply and Demand

The IEA (1) downgraded their 2021 and 2022 demand estimates by 100,000 bbl/day to reflect what they think will be a limited impact on oil demand from the Omicron variant. This sees demand at 96.4 MMbbl/day and 99.7 MMbbl/day in 2021 and 2022 respectively. The EIA (2) was less sanguine, shaving 500,000 bbl/day off their 2022 demand estimate to bring it down to 100.4 MMbbl/day and signaled that the uncertainty around the path Omicron takes could see further revision over the coming months. This may reflect some revision to historical data as they also lowered their 2021 demand estimate from 97.5 MMbbl/day to 96.9 MMbbl/day month over month. OPEC (3) held their 2021 and 2022 demand estimates steady at 97.7 MMbbl/day and 100.6 MMbbl/day respectively.

On the supply side, the last month saw a release from the US Strategic Petroleum Reserve in co-ordination with several other nations – Japan, China and South Korea. The volumes committed were nominal – 50 MMbbl by the US, which is about 12 hours of global demand – and did little to affect the market. There had been a suggestion that the OPEC+ group of nations would respond by reversing their decision to raise production quotas in December, but in the event that did not happen. At their meeting of the 2nd of December (4), the OPEC+ group of nations agreed that they would maintain their 400,000 bbl/day December increase as planned and add a further 400,000 bbl/day in January 2022.

While OPEC+ is currently holding course with a measured return of production, high oil prices and a return to pre-pandemic quota levels are starting to reveal divergent dynamics within the group. As mentioned last month, Kuwait’s underlying production capacity has declined and both Nigeria and Angola have struggled to reach their pandemic reduced quotas over recent months (5). On the other hand, Russia has indicated that it is ready to return to full production capacity and Iran has announced that it intends to raise its production to its pre-sanction level of 4 MMbbl/day by March 2022 (6). These tensions suggest that maintaining the discipline and unity that has been the hallmark of the OPEC+ meetings for the last 18 months may become increasingly difficult as production levels return to normal in mid 2022.

Recent capital budget announcements by two International Oil Companies (IOC’s) have not indicated a willingness to return to pre-pandemic investment levels (7). In a reversal of its pre-pandemic strategy, Exxon committed to a reduced capital budget of $20 - $25 billion per annum through 2027, while Chevron committed to $15 billion per annum through 2025. This constitutes a 17% - 33% reduction for Exxon and a 25% reduction for Chevron against pre-pandemic levels.

All three agencies are now predicting a supply surplus in 2022, with a return of both OPEC and non-OPEC supply. The IEA predicts that Canada, Brazil, the US, Russia and Saudi Arabia will all hit new production records next year. Our own model shows the market to be in a small surplus for 2022, with a large surplus in the first half of the year largely offset by a deficit in the second half. The major difference between our own forecast and that of the main agencies is in US production; we predict the US will add about 200,000 bbl/day next year whereas all three agencies are predicting much stronger US production growth. Our forecast is shown in Figure 1, below.

Figure 1 - Supply and Demand Surplus Forecast

Oil Storage

We estimate global oil inventory drawdowns of 322 MMbbl in 2021, flipping to a surplus of 66 MMbbl in 2022 as OPEC+ returns to reference production levels. Figure 2 shows global storage capacity and inventories. If supply and demand follow the current forecast, global inventories will be around the five-year average for the 4th quarter 2021 and remain about that level through 2022 and 2023.

Figure 2 - Global Storage Chart

Oil Prices

Omicron achieved what a coordinated release of oil from national strategic reserves failed to with oil prices dropping sharply over the last month. WTI fell from near $85/bbl last month to $65/bbl before bouncing back to just above $70/bbl at the time of writing. The EIA is now predicting downward price pressure in 2022, as stocks start to build again. They are forecasting a Brent average price of $73/barrel in Q1 next year falling to $67/bbl by Q4.

Both Brent and WTI futures fell, with steeper near term falls. Brent remains close to $65/bbl out to the end of the decade, with WTI close to $60/bbl.

Figure 3 - Brent Crude Oil Futures

Figure 4 - WTI Crude Oil Futures

US Activity

As OPEC+ returns production to normal next year, US production will once more move to center stage in determining oil market balance. The US land oil rig count continued to rise this month, reaching 459 on the 17th of December. We expect it to average 365 for 2021, up slightly from the 321 count of 2020, but still down sharply from the 753 average of 2019.

Figure 5 - US Land Oil Rig Count

We expect US production to average 16.4 MMbbl/day for 2021, down slightly from 2020. Our guestimate is that US onshore capital budgets will rise by about 20% next year in real terms, which would equate to an average rig count of about 440 for the year, around current activity levels. This would be enough to boost production by ~ 200,000 bbl/day to 16.6 MMbbl/day in 2022.

As noted in the Supply and Demand section, the IEA are predicting US production in 2022 will exceed its record 2019 level of 17.2 MMbbl/day. According to our model, to raise average US production in 2022 by 900,000 bbl/day would require an average 2022 oil land rig count of 570, suggesting rig counts at 2019 levels by the end of 2022. That would imply a CAPEX budget increase of 60% year on year, which doesn’t seem consistent with the current philosophy of profits over production.

(1) Oil Market Report – December 2021, International Energy Agency

(2) Short Term Energy Outlook (STEO), December 2nd, 2021, U.S. Energy Information Administration.

(3) “OPEC Monthly Oil Market Report”, Organization of the Petroleum Exporting Countries, November 11th, 2021.

(4) 23rd OPEC and Non-OPEC Ministerial Meeting, December 2nd, 2021.

(5) “Russia Is Ready to Return to Pre-Pandemic Oil Production”, Tsvetana Paraskova, Oilprice.com, November 29th, 2021.

(6) “Iran seeks to return oil output to pre-sanction levels”, Arsalan Shahla, World Oil, November 28th, 2021

(7) “Exxon to Continue Leaner Spending as Covid-19 Threat Lingers”, Christopher Matthews, December 1st, Wall Street Journal.

Explore Our Services

Business Development

Oil & Gas an extractive industry, participants must continuously find and develop new oil & gas fields as existing fields decline, making business development a continuous process.

Strategy

We approach strategy through a scenario driven assessment of the client’s current portfolio, organizational competencies, and financial framework. The strategy defines portfolio actions and coveted asset attributes.

Origination

Deal origination consists of identifying coveted assets, assets with attributes consistent with the client’s strategy, and qualified buyers. We advocate a proactive approach to business development and will undertake outreach on our client’s behalf.

Transaction Support

Transaction support consists of in depth asset evaluation, negotiation of commercial agreements or preparation of license round submission and close out of conditions. We can also aid in joint venture set up and management and asset maturation as required.